Importance Sampling Examples

from qmcpy import *

from numpy import *

import pandas as pd

pd.options.display.float_format = '{:.2e}'.format

from matplotlib import pyplot as plt

import matplotlib

%matplotlib inline

Game Example

Consider a game where

are drawn

with a payoff of

are drawn

with a payoff of

What is the expected payoff of this game?

payoff = lambda x: 10*(x.sum(1)>1.7)

abs_tol = 1e-3

Vanilla Monte Carlo

With ordinary Monte Carlo we do the following:

![\mu = \mathbb{E}(Y) = \int_{[0,1]^2} \text{payoff}(x_1,x_2) \,

\mathrm{d} x_1 \mathrm{d}x_2](../_images/math/adc2df06b15cf8ac84142b29e01db67710c12ff3.png)

d = 2

integral = CustomFun(

true_measure = Uniform(Lattice(d)),

g = payoff)

solution1,data1 = CubQMCLatticeG(integral, abs_tol).integrate()

data1

LDTransformData (AccumulateData Object)

solution 0.450

comb_bound_low 0.449

comb_bound_high 0.450

comb_flags 1

n_total 2^(16)

n 2^(16)

time_integrate 0.043

CubQMCLatticeG (StoppingCriterion Object)

abs_tol 0.001

rel_tol 0

n_init 2^(10)

n_max 2^(35)

CustomFun (Integrand Object)

Uniform (TrueMeasure Object)

lower_bound 0

upper_bound 1

Lattice (DiscreteDistribution Object)

d 2^(1)

dvec [0 1]

randomize 1

order natural

entropy 260768472417330885254602359583380448047

spawn_key ()

Monte Carlo with Importance Sampling

We may add the importance sampling to increase the number of samples with positive payoffs. Let

This means that  and

and  are IID with common CDF

are IID with common CDF

and common PDF

and common PDF  .

Thus,

.

Thus,

![\mu = \mathbb{E}(Y) = \int_{[0,1]^2} \frac{\text{payoff}(z_1,z_2)}{(p+1)^2(z_1z_2)^{p}} \, \varrho(z_1)

\varrho(z_2) \, \mathrm{d} z_1 \mathrm{d}z_2 \\

= \int_{[0,1]^2}

\frac{\text{payoff}(x_1^{1/(p+1)},x_2^{1/(p+1)})}{(p+1)^2(x_1x_2)^{p/(p+1)}}

\, \mathrm{d} x_1 \mathrm{d}x_2](../_images/math/c29707dbb0b59193c3ddb9391cd7f98e0ddb6c91.png)

p = 1

d = 2

integral = CustomFun(

true_measure = Uniform(Lattice(d)),

g = lambda x: payoff(x**(1/(p+1))) / ((p+1)**2 * (x.prod(1))**(p/(p+1))))

solution2,data2 = CubQMCLatticeG(integral, abs_tol).integrate()

data2

LDTransformData (AccumulateData Object)

solution 0.451

comb_bound_low 0.450

comb_bound_high 0.451

comb_flags 1

n_total 2^(14)

n 2^(14)

time_integrate 0.019

CubQMCLatticeG (StoppingCriterion Object)

abs_tol 0.001

rel_tol 0

n_init 2^(10)

n_max 2^(35)

CustomFun (Integrand Object)

Uniform (TrueMeasure Object)

lower_bound 0

upper_bound 1

Lattice (DiscreteDistribution Object)

d 2^(1)

dvec [0 1]

randomize 1

order natural

entropy 101794984569737015308869089738144162915

spawn_key ()

print('Imporance Sampling takes %.3f the time and %.3f the samples'%\

(data2.time_integrate/data1.time_integrate,data2.n_total/data1.n_total))

Imporance Sampling takes 0.451 the time and 0.250 the samples

Asian Call Option Example

The stock price must raise significantly for the payoff to be positive. So we will give an upward drift to the Brownian motion that defines the stock price path. We can think of the option price as the multidimensional integral

![\mu = \mathbb{E}[f(\boldsymbol{X})] = \int_{\mathbb{R}^d}

f(\boldsymbol{x})

\frac{\exp\bigl(-\frac{1}{2} \boldsymbol{x}^T\mathsf{\Sigma}^{-1}

\boldsymbol{x}\bigr)}

{\sqrt{(2 \pi)^{d} \det(\mathsf{\Sigma})}} \, \mathrm{d} \boldsymbol{x}](../_images/math/8c3ec0f4f51d93f6048cefc5928785f5c31703a2.png)

where

We will replace  by

by

where a positive  will create more positive payoffs. This

corresponds to giving our Brownian motion a drift. To do this we

re-write the integral as

will create more positive payoffs. This

corresponds to giving our Brownian motion a drift. To do this we

re-write the integral as

![\mu = \mathbb{E}[f_{\mathrm{new}}(\boldsymbol{Z})]

= \int_{\mathbb{R}^d}

f_{\mathrm{new}}(\boldsymbol{z})

\frac{\exp\bigl(-\frac{1}{2} (\boldsymbol{z}-\boldsymbol{a})^T

\mathsf{\Sigma}^{-1}

(\boldsymbol{z} - \boldsymbol{a}) \bigr)}

{\sqrt{(2 \pi)^{d} \det(\mathsf{\Sigma})}} \, \mathrm{d} \boldsymbol{z} ,

\\

f_{\mathrm{new}}(\boldsymbol{z}) =

f(\boldsymbol{z})

\frac{\exp\bigl(-\frac{1}{2} \boldsymbol{z}^T

\mathsf{\Sigma}^{-1} \boldsymbol{z} \bigr)}

{\exp\bigl(-\frac{1}{2} (\boldsymbol{z}-\boldsymbol{a})^T

\mathsf{\Sigma}^{-1}

(\boldsymbol{z} - \boldsymbol{a}) \bigr)}

= f(\boldsymbol{z}) \exp\bigl((\boldsymbol{a}/2 - \boldsymbol{z})^T

\mathsf{\Sigma}^{-1}\boldsymbol{a} \bigr)](../_images/math/1d7a80e9501fc67e7507cc1b638e91c9094238e6.png)

Finally note that

This drift in the Brownian motion may be implemented by changing the

drift input to the BrownianMotion object.

abs_tol = 1e-2

dimension = 32

Vanilla Monte Carlo

integrand = AsianOption(Sobol(dimension))

solution1,data1 = CubQMCSobolG(integrand, abs_tol).integrate()

data1

LDTransformData (AccumulateData Object)

solution 1.788

comb_bound_low 1.782

comb_bound_high 1.794

comb_flags 1

n_total 2^(12)

n 2^(12)

time_integrate 0.014

CubQMCSobolG (StoppingCriterion Object)

abs_tol 0.010

rel_tol 0

n_init 2^(10)

n_max 2^(35)

AsianOption (Integrand Object)

volatility 2^(-1)

call_put call

start_price 30

strike_price 35

interest_rate 0

mean_type arithmetic

dim_frac 0

BrownianMotion (TrueMeasure Object)

time_vec [0.031 0.062 0.094 ... 0.938 0.969 1. ]

drift 0

mean [0. 0. 0. ... 0. 0. 0.]

covariance [[0.031 0.031 0.031 ... 0.031 0.031 0.031]

[0.031 0.062 0.062 ... 0.062 0.062 0.062]

[0.031 0.062 0.094 ... 0.094 0.094 0.094]

...

[0.031 0.062 0.094 ... 0.938 0.938 0.938]

[0.031 0.062 0.094 ... 0.938 0.969 0.969]

[0.031 0.062 0.094 ... 0.938 0.969 1. ]]

decomp_type PCA

Sobol (DiscreteDistribution Object)

d 2^(5)

dvec [ 0 1 2 ... 29 30 31]

randomize LMS_DS

graycode 0

entropy 296048682239793520955192894339316320391

spawn_key ()

Monte Carlo with Importance Sampling

drift = 1

integrand = AsianOption(BrownianMotion(Sobol(dimension),drift=drift))

solution2,data2 = CubQMCSobolG(integrand, abs_tol).integrate()

data2

LDTransformData (AccumulateData Object)

solution 1.783

comb_bound_low 1.776

comb_bound_high 1.790

comb_flags 1

n_total 2^(11)

n 2^(11)

time_integrate 0.014

CubQMCSobolG (StoppingCriterion Object)

abs_tol 0.010

rel_tol 0

n_init 2^(10)

n_max 2^(35)

AsianOption (Integrand Object)

volatility 2^(-1)

call_put call

start_price 30

strike_price 35

interest_rate 0

mean_type arithmetic

dim_frac 0

BrownianMotion (TrueMeasure Object)

time_vec [0.031 0.062 0.094 ... 0.938 0.969 1. ]

drift 0

mean [0. 0. 0. ... 0. 0. 0.]

covariance [[0.031 0.031 0.031 ... 0.031 0.031 0.031]

[0.031 0.062 0.062 ... 0.062 0.062 0.062]

[0.031 0.062 0.094 ... 0.094 0.094 0.094]

...

[0.031 0.062 0.094 ... 0.938 0.938 0.938]

[0.031 0.062 0.094 ... 0.938 0.969 0.969]

[0.031 0.062 0.094 ... 0.938 0.969 1. ]]

decomp_type PCA

transform BrownianMotion (TrueMeasure Object)

time_vec [0.031 0.062 0.094 ... 0.938 0.969 1. ]

drift 1

mean [0.031 0.062 0.094 ... 0.938 0.969 1. ]

covariance [[0.031 0.031 0.031 ... 0.031 0.031 0.031]

[0.031 0.062 0.062 ... 0.062 0.062 0.062]

[0.031 0.062 0.094 ... 0.094 0.094 0.094]

...

[0.031 0.062 0.094 ... 0.938 0.938 0.938]

[0.031 0.062 0.094 ... 0.938 0.969 0.969]

[0.031 0.062 0.094 ... 0.938 0.969 1. ]]

decomp_type PCA

Sobol (DiscreteDistribution Object)

d 2^(5)

dvec [ 0 1 2 ... 29 30 31]

randomize LMS_DS

graycode 0

entropy 144971093458566807495711477416245436939

spawn_key ()

print('Imporance Sampling takes %.3f the time and %.3f the samples'%\

(data2.time_integrate/data1.time_integrate,data2.n_total/data1.n_total))

Imporance Sampling takes 1.009 the time and 0.500 the samples

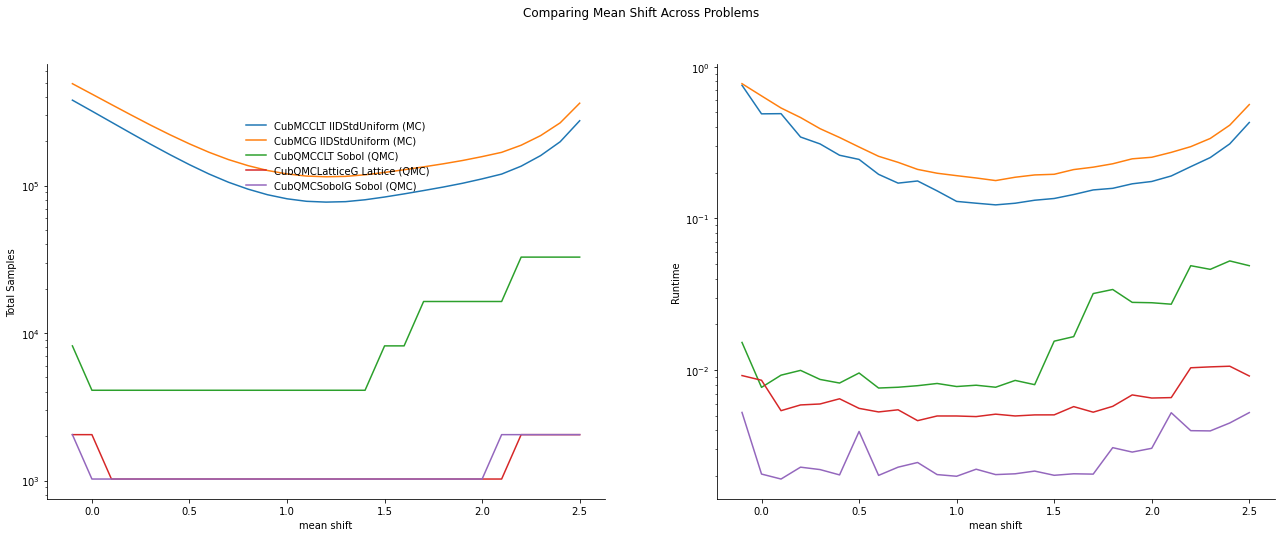

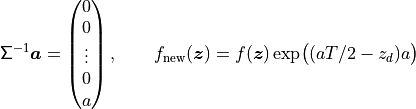

Importance Sampling MC vs QMC

Test Parameters

dimension = 16

abs_tol = .025

trials = 3

df = pd.read_csv('../workouts/mc_vs_qmc/out/importance_sampling.csv')

df['Problem'] = df['Stopping Criterion'] + ' ' + df['Distribution'] + ' (' + df['MC/QMC'] + ')'

df = df.drop(['Stopping Criterion','Distribution','MC/QMC'],axis=1)

problems = ['CubMCCLT IIDStdUniform (MC)',

'CubMCG IIDStdUniform (MC)',

'CubQMCCLT Sobol (QMC)',

'CubQMCLatticeG Lattice (QMC)',

'CubQMCSobolG Sobol (QMC)']

df = df[df['Problem'].isin(problems)]

mean_shifts = df.mean_shift.unique()

df_samples = df.groupby(['Problem'])['n_samples'].apply(list).reset_index(name='n')

df_times = df.groupby(['Problem'])['time'].apply(list).reset_index(name='time')

df.loc[(df.mean_shift==0) | (df.mean_shift==1)].set_index('Problem')

# Note: mean_shift==0 --> NOT using importance sampling

| mean_shift | solution | n_samples | time | |

|---|---|---|---|---|

| Problem | ||||

| CubMCCLT IIDStdUniform (MC) | 0.00e+00 | 1.80e+00 | 3.20e+05 | 4.90e-01 |

| CubMCCLT IIDStdUniform (MC) | 1.00e+00 | 1.77e+00 | 8.15e+04 | 1.30e-01 |

| CubMCG IIDStdUniform (MC) | 0.00e+00 | 1.80e+00 | 4.18e+05 | 6.43e-01 |

| CubMCG IIDStdUniform (MC) | 1.00e+00 | 1.77e+00 | 1.20e+05 | 1.91e-01 |

| CubQMCCLT Sobol (QMC) | 0.00e+00 | 1.78e+00 | 4.10e+03 | 7.69e-03 |

| CubQMCCLT Sobol (QMC) | 1.00e+00 | 1.78e+00 | 4.10e+03 | 7.79e-03 |

| CubQMCLatticeG Lattice (QMC) | 0.00e+00 | 1.78e+00 | 2.05e+03 | 8.56e-03 |

| CubQMCLatticeG Lattice (QMC) | 1.00e+00 | 1.78e+00 | 1.02e+03 | 4.98e-03 |

| CubQMCSobolG Sobol (QMC) | 0.00e+00 | 1.78e+00 | 1.02e+03 | 2.06e-03 |

| CubQMCSobolG Sobol (QMC) | 1.00e+00 | 1.78e+00 | 1.02e+03 | 1.99e-03 |

fig,ax = plt.subplots(nrows=1, ncols=2, figsize=(20, 6))

idx = arange(len(problems))

width = .35

ax[0].barh(idx+width,log(df.loc[df.mean_shift==0]['n_samples'].values),width)

ax[0].barh(idx,log(df.loc[df.mean_shift==1]['n_samples'].values),width)

ax[1].barh(idx+width,df.loc[df.mean_shift==0]['time'].values,width)

ax[1].barh(idx,df.loc[df.mean_shift==1]['time'].values,width)

fig.suptitle('Importance Sampling Comparison by Stopping Criterion on Asian Call Option')

xlabs = ['log(Samples)','Time']

for i in range(len(ax)):

ax[i].set_xlabel(xlabs[i])

ax[i].spines['top'].set_visible(False)

ax[i].spines['bottom'].set_visible(False)

ax[i].spines['right'].set_visible(False)

ax[i].spines['left'].set_visible(False)

ax[1].legend(['Vanilla Monte Carlo','Importance Sampling\nMean Shift=1'],loc='upper right',frameon=False)

ax[1].get_yaxis().set_ticks([])

ax[0].set_yticks(idx)

ax[0].set_yticklabels(problems)

plt.tight_layout();

fig,ax = plt.subplots(nrows=1, ncols=2, figsize=(22, 8))

df_samples.apply(lambda row: ax[0].plot(mean_shifts,row.n,label=row['Problem']),axis=1)

df_times.apply(lambda row: ax[1].plot(mean_shifts,row.time,label=row['Problem']),axis=1)

ax[1].legend(frameon=False, loc=(-.85,.7),ncol=1)

ax[0].set_ylabel('Total Samples')

ax[0].set_yscale('log')

ax[1].set_yscale('log')

ax[1].set_ylabel('Runtime')

for i in range(len(ax)):

ax[i].set_xlabel('mean shift')

ax[i].spines['top'].set_visible(False)

ax[i].spines['right'].set_visible(False)

fig.suptitle('Comparing Mean Shift Across Problems');