QMCPy Documentation

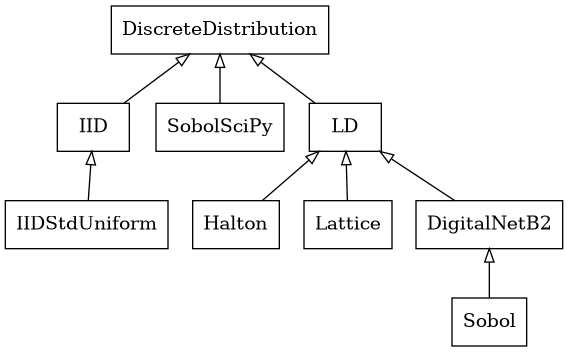

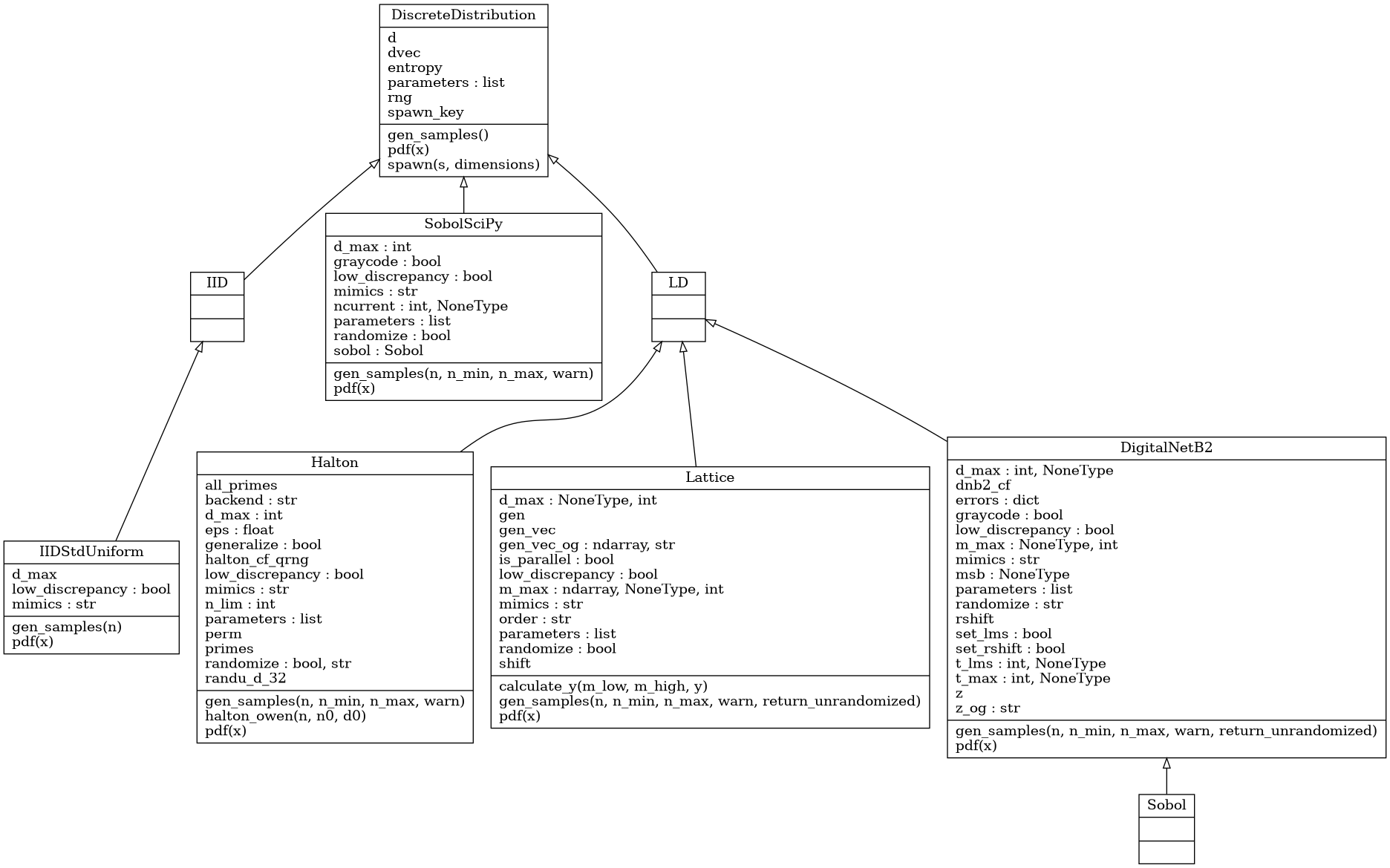

Discrete Distribution Class

Abstract Discrete Distribution Class

- class qmcpy.discrete_distribution._discrete_distribution.DiscreteDistribution(dimension, seed)

Discrete Distribution abstract class. DO NOT INSTANTIATE.

- __init__(dimension, seed)

- Parameters

dimension (int or ndarray) – dimension of the generator. If an int is passed in, use sequence dimensions [0,…,dimensions-1]. If a ndarray is passed in, use these dimension indices in the sequence. Note that this is not relevant for IID generators.

seed (int or numpy.random.SeedSequence) – seed to create random number generator

- gen_samples(*args)

ABSTRACT METHOD to generate samples from this discrete distribution.

- Parameters

args (tuple) – tuple of positional argument. See implementations for details

- Returns

n x d array of samples

- Return type

ndarray

- pdf(x)

ABSTRACT METHOD to evaluate pdf of distribution the samples mimic at locations of x.

- spawn(s=1, dimensions=None)

Spawn new instances of the current discrete distribution but with new seeds and dimensions. Developed for multi-level and multi-replication (Q)MC algorithms.

- class qmcpy.discrete_distribution._discrete_distribution.IID(dimension, seed)

- class qmcpy.discrete_distribution._discrete_distribution.LD(dimension, seed)

Digital Net Base 2

- class qmcpy.discrete_distribution.digital_net_b2.digital_net_b2.DigitalNetB2(dimension=1, randomize='LMS_DS', graycode=False, seed=None, generating_matrices='sobol_mat.21201.32.32.msb.npy', d_max=None, t_max=None, m_max=None, msb=None, t_lms=None, _verbose=False)

Quasi-Random digital nets in base 2.

>>> dnb2 = DigitalNetB2(2,seed=7) >>> dnb2.gen_samples(4) array([[0.56269008, 0.17377997], [0.346653 , 0.65070632], [0.82074548, 0.95490574], [0.10422261, 0.49458097]]) >>> dnb2.gen_samples(1) array([[0.56269008, 0.17377997]]) >>> dnb2 DigitalNetB2 (DiscreteDistribution Object) d 2^(1) dvec [0 1] randomize LMS_DS graycode 0 entropy 7 spawn_key () >>> DigitalNetB2(dimension=2,randomize=False,graycode=True).gen_samples(n_min=2,n_max=4) array([[0.75, 0.25], [0.25, 0.75]]) >>> DigitalNetB2(dimension=2,randomize=False,graycode=False).gen_samples(n_min=2,n_max=4) array([[0.25, 0.75], [0.75, 0.25]]) >>> dnb2_alpha2 = DigitalNetB2(5,randomize=False,generating_matrices='sobol_mat_alpha2.10600.64.32.lsb.npy') >>> dnb2_alpha2.gen_samples(8,warn=False) array([[0. , 0. , 0. , 0. , 0. ], [0.75 , 0.75 , 0.75 , 0.75 , 0.75 ], [0.4375 , 0.9375 , 0.1875 , 0.6875 , 0.1875 ], [0.6875 , 0.1875 , 0.9375 , 0.4375 , 0.9375 ], [0.296875, 0.171875, 0.109375, 0.796875, 0.859375], [0.546875, 0.921875, 0.859375, 0.046875, 0.109375], [0.234375, 0.859375, 0.171875, 0.484375, 0.921875], [0.984375, 0.109375, 0.921875, 0.734375, 0.171875]])

References

[1] Marius Hofert and Christiane Lemieux (2019). qrng: (Randomized) Quasi-Random Number Generators. R package version 0.0-7. https://CRAN.R-project.org/package=qrng.

[2] Faure, Henri, and Christiane Lemieux. “Implementation of Irreducible Sobol’ Sequences in Prime Power Bases.” Mathematics and Computers in Simulation 161 (2019): 13-22. Crossref. Web.

[3] F.Y. Kuo & D. Nuyens. Application of quasi-Monte Carlo methods to elliptic PDEs with random diffusion coefficients - a survey of analysis and implementation, Foundations of Computational Mathematics, 16(6):1631-1696, 2016. springer link: https://link.springer.com/article/10.1007/s10208-016-9329-5 arxiv link: https://arxiv.org/abs/1606.06613

[4] D. Nuyens, The Magic Point Shop of QMC point generators and generating vectors. MATLAB and Python software, 2018. Available from https://people.cs.kuleuven.be/~dirk.nuyens/ https://bitbucket.org/dnuyens/qmc-generators/src/cb0f2fb10fa9c9f2665e41419097781b611daa1e/cpp/digitalseq_b2g.hpp

[5] Paszke, A., Gross, S., Massa, F., Lerer, A., Bradbury, J., Chanan, G., … Chintala, S. (2019). PyTorch: An Imperative Style, High-Performance Deep Learning Library. In H. Wallach, H. Larochelle, A. Beygelzimer, F. d extquotesingle Alch'e-Buc, E. Fox, & R. Garnett (Eds.), Advances in Neural Information Processing Systems 32 (pp. 8024-8035). Curran Associates, Inc. Retrieved from http://papers.neurips.cc/paper/9015-pytorch-an-imperative-style-high-performance-deep-learning-library.pdf

[6] I.M. Sobol’, V.I. Turchaninov, Yu.L. Levitan, B.V. Shukhman: “Quasi-Random Sequence Generators” Keldysh Institute of Applied Mathematics, Russian Acamdey of Sciences, Moscow (1992).

[7] Sobol, Ilya & Asotsky, Danil & Kreinin, Alexander & Kucherenko, Sergei. (2011). Construction and Comparison of High-Dimensional Sobol’ Generators. Wilmott. 2011. 10.1002/wilm.10056.

[8] Paul Bratley and Bennett L. Fox. 1988. Algorithm 659: Implementing Sobol’s quasirandom sequence generator. ACM Trans. Math. Softw. 14, 1 (March 1988), 88-100. DOI:https://doi.org/10.1145/42288.214372

- __init__(dimension=1, randomize='LMS_DS', graycode=False, seed=None, generating_matrices='sobol_mat.21201.32.32.msb.npy', d_max=None, t_max=None, m_max=None, msb=None, t_lms=None, _verbose=False)

- Parameters

dimension (int or ndarray) – dimension of the generator. If an int is passed in, use sequence dimensions [0,…,dimensions-1]. If a ndarray is passed in, use these dimension indices in the sequence.

randomize (bool) – apply randomization? True defaults to LMS_DS. Can also explicitly pass in ‘LMS_DS’: linear matrix scramble with digital shift ‘LMS’: linear matrix scramble only ‘DS’: digital shift only

graycode (bool) – indicator to use graycode ordering (True) or natural ordering (False)

seed (list) – int seed of list of seeds, one for each dimension.

generating_matrices (ndarray or str) – generating matrices or path to generating matrices. ndarray should have shape (d_max, m_max) where each int has t_max bits generating_matrices should be formatted like gen_mat.21201.32.32.msb.npy with name.d_max.t_max.m_max.{msb,lsb}.npy

d_max (int) – max dimension

t_max (int) – number of bits in each int of each generating matrix. aka: number of rows in a generating matrix with ints expanded into columns

m_max (int) – 2^m_max is the number of samples supported. aka: number of columns in a generating matrix with ints expanded into columns

msb (bool) – bit storage as ints. e.g. if t_max=3, then 6 is [1 1 0] in MSB (True) and [0 1 1] in LSB (False)

t_lms (int) – LMS scrambling matrix will be t_lms x t_max for generating matrix of shape t_max x m_max

_verbose (bool) – print randomization details

- gen_samples(n=None, n_min=0, n_max=8, warn=True, return_unrandomized=False)

Generate samples

- Parameters

n (int) – if n is supplied, generate from n_min=0 to n_max=n samples. Otherwise use the n_min and n_max explicitly supplied as the following 2 arguments

n_min (int) – Starting index of sequence.

n_max (int) – Final index of sequence.

return_unrandomized (bool) – return unrandomized samples as well? If True, return randomized_samples,unrandomized_samples. Note that this only applies when randomize includes Digital Shift. Also note that unrandomized samples included linear matrix scrambling if applicable.

- Returns

(n_max-n_min) x d (dimension) array of samples

- Return type

ndarray

- pdf(x)

pdf of a standard uniform

- class qmcpy.discrete_distribution.digital_net_b2.digital_net_b2.Sobol(dimension=1, randomize='LMS_DS', graycode=False, seed=None, generating_matrices='sobol_mat.21201.32.32.msb.npy', d_max=None, t_max=None, m_max=None, msb=None, t_lms=None, _verbose=False)

Lattice

- class qmcpy.discrete_distribution.lattice.lattice.Lattice(dimension=1, randomize=True, order='natural', seed=None, generating_vector='lattice_vec.3600.20.npy', d_max=None, m_max=None, is_parallel=True)

Quasi-Random Lattice nets in base 2.

>>> l = Lattice(2,seed=7) >>> l.gen_samples(4) array([[0.04386058, 0.58727432], [0.54386058, 0.08727432], [0.29386058, 0.33727432], [0.79386058, 0.83727432]]) >>> l.gen_samples(1) array([[0.04386058, 0.58727432]]) >>> l Lattice (DiscreteDistribution Object) d 2^(1) dvec [0 1] randomize 1 order natural gen_vec [ 1 182667] entropy 7 spawn_key () >>> Lattice(dimension=2,randomize=False,order='natural').gen_samples(4, warn=False) array([[0. , 0. ], [0.5 , 0.5 ], [0.25, 0.75], [0.75, 0.25]]) >>> Lattice(dimension=2,randomize=False,order='linear').gen_samples(4, warn=False) array([[0. , 0. ], [0.25, 0.75], [0.5 , 0.5 ], [0.75, 0.25]]) >>> Lattice(dimension=2,randomize=False,order='mps').gen_samples(4, warn=False) array([[0. , 0. ], [0.5 , 0.5 ], [0.25, 0.75], [0.75, 0.25]]) >>> l = Lattice(2,generating_vector=25,seed=55) >>> l.gen_samples(4) array([[0.84489224, 0.30534549], [0.34489224, 0.80534549], [0.09489224, 0.05534549], [0.59489224, 0.55534549]]) >>> l Lattice (DiscreteDistribution Object) d 2^(1) dvec [0 1] randomize 1 order natural gen_vec [ 1 11961679] entropy 55 spawn_key () >>> Lattice(dimension=4,randomize=False,seed=353,generating_vector=26).gen_samples(8,warn=False) array([[0. , 0. , 0. , 0. ], [0.5 , 0.5 , 0.5 , 0.5 ], [0.25 , 0.25 , 0.75 , 0.75 ], [0.75 , 0.75 , 0.25 , 0.25 ], [0.125, 0.125, 0.875, 0.875], [0.625, 0.625, 0.375, 0.375], [0.375, 0.375, 0.625, 0.625], [0.875, 0.875, 0.125, 0.125]]) >>> Lattice(dimension=4,randomize=False,seed=353,generating_vector=26,is_parallel=True).gen_samples(8,warn=False) array([[0. , 0. , 0. , 0. ], [0.5 , 0.5 , 0.5 , 0.5 ], [0.25 , 0.25 , 0.75 , 0.75 ], [0.75 , 0.75 , 0.25 , 0.25 ], [0.125, 0.125, 0.875, 0.875], [0.625, 0.625, 0.375, 0.375], [0.375, 0.375, 0.625, 0.625], [0.875, 0.875, 0.125, 0.125]])

References

[1] Sou-Cheng T. Choi, Yuhan Ding, Fred J. Hickernell, Lan Jiang, Lluis Antoni Jimenez Rugama, Da Li, Jagadeeswaran Rathinavel, Xin Tong, Kan Zhang, Yizhi Zhang, and Xuan Zhou, GAIL: Guaranteed Automatic Integration Library (Version 2.3) [MATLAB Software], 2019. Available from http://gailgithub.github.io/GAIL_Dev/

[2] F.Y. Kuo & D. Nuyens. Application of quasi-Monte Carlo methods to elliptic PDEs with random diffusion coefficients - a survey of analysis and implementation, Foundations of Computational Mathematics, 16(6):1631-1696, 2016. springer link: https://link.springer.com/article/10.1007/s10208-016-9329-5 arxiv link: https://arxiv.org/abs/1606.06613

[3] D. Nuyens, The Magic Point Shop of QMC point generators and generating vectors. MATLAB and Python software, 2018. Available from https://people.cs.kuleuven.be/~dirk.nuyens/

[4] Constructing embedded lattice rules for multivariate integration R Cools, FY Kuo, D Nuyens - SIAM J. Sci. Comput., 28(6), 2162-2188.

[5] L’Ecuyer, Pierre & Munger, David. (2015). LatticeBuilder: A General Software Tool for Constructing Rank-1 Lattice Rules. ACM Transactions on Mathematical Software. 42. 10.1145/2754929.

- __init__(dimension=1, randomize=True, order='natural', seed=None, generating_vector='lattice_vec.3600.20.npy', d_max=None, m_max=None, is_parallel=True)

- Parameters

dimension (int or ndarray) – dimension of the generator. If an int is passed in, use sequence dimensions [0,…,dimensions-1]. If a ndarray is passed in, use these dimension indices in the sequence.

randomize (bool) – If True, apply shift to generated samples. Note: Non-randomized lattice sequence includes the origin.

order (str) – ‘linear’, ‘natural’, or ‘mps’ ordering.

seed (None or int or numpy.random.SeedSeq) – seed the random number generator for reproducibility

generating_vector (ndarray, str or int) – generating matrix or path to generating matrices. ndarray should have shape (d_max). a string generating_vector should be formatted like ‘lattice_vec.3600.20.npy’ where ‘name.d_max.m_max.npy’ an integer should be an odd larger than 1; passing an integer M would create a random generating vector supporting up to 2^M points. M is restricted between 2 and 26 for numerical percision. The generating vector is [1,v_1,v_2,…,v_dimension], where v_i is an integer in {3,5,…,2*M-1}.

d_max (int) – maximum dimension

m_max (int) – 2^m_max is the max number of supported samples

is_parallel (bool) – Default to True to perform parallel computations, False serial

Note

d_max and m_max are required if generating_vector is a ndarray. If generating_vector is an string (path), d_max and m_max can be taken from the file name if None

- gen_samples(n=None, n_min=0, n_max=8, warn=True, return_unrandomized=False)

Generate lattice samples

- Parameters

n (int) – if n is supplied, generate from n_min=0 to n_max=n samples. Otherwise use the n_min and n_max explicitly supplied as the following 2 arguments

n_min (int) – Starting index of sequence.

n_max (int) – Final index of sequence.

return_unrandomized (bool) – return samples without randomization as 2nd return value. Will not be returned if randomize=False.

- Returns

(n_max-n_min) x d (dimension) array of samples

- Return type

ndarray

Note

Lattice generates in blocks from 2**m to 2**(m+1) so generating n_min=3 to n_max=9 requires necessarily produces samples from n_min=2 to n_max=16 and automatically subsets. May be inefficient for non-powers-of-2 samples sizes.

- pdf(x)

pdf of a standard uniform

Halton

- class qmcpy.discrete_distribution.halton.Halton(dimension=1, randomize=True, generalize=True, seed=None)

Quasi-Random Halton nets.

>>> h_qrng = Halton(2,randomize='QRNG',generalize=True,seed=7) >>> h_qrng.gen_samples(4) array([[0.35362988, 0.38733489], [0.85362988, 0.72066823], [0.10362988, 0.05400156], [0.60362988, 0.498446 ]]) >>> h_qrng.gen_samples(1) array([[0.35362988, 0.38733489]]) >>> h_qrng Halton (DiscreteDistribution Object) d 2^(1) dvec [0 1] randomize QRNG generalize 1 entropy 7 spawn_key () >>> h_owen = Halton(2,randomize='OWEN',generalize=False,seed=7) >>> h_owen.gen_samples(4) array([[0.64637012, 0.48226667], [0.14637012, 0.81560001], [0.89637012, 0.14893334], [0.39637012, 0.59337779]]) >>> h_owen Halton (DiscreteDistribution Object) d 2^(1) dvec [0 1] randomize OWEN generalize 0 entropy 7 spawn_key ()

References

[1] Marius Hofert and Christiane Lemieux (2019). qrng: (Randomized) Quasi-Random Number Generators. R package version 0.0-7. https://CRAN.R-project.org/package=qrng.

[2] Owen, A. B. “A randomized Halton algorithm in R,” 2017. arXiv:1706.02808 [stat.CO]

- __init__(dimension=1, randomize=True, generalize=True, seed=None)

- Parameters

dimension (int or ndarray) – dimension of the generator. If an int is passed in, use sequence dimensions [0,…,dimensions-1]. If a ndarray is passed in, use these dimension indices in the sequence.

randomize (str/bool) – select randomization method from ‘QRNG” [1], (max dimension = 360, supports generalize=True, default if randomize=True) or ‘OWEN’ [2], (max dimension = 1000),

generalize (bool) – generalize flag, only applicable to the QRNG generator

seed (None or int or numpy.random.SeedSeq) – seed the random number generator for reproducibility

- gen_samples(n=None, n_min=0, n_max=8, warn=True)

Generate samples

- Parameters

- Returns

(n_max-n_min) x d (dimension) array of samples

- Return type

ndarray

- halton_owen(n, n0, d0=0)

see gen_samples method and [1] Owen, A. B.A randomized Halton algorithm in R2017. arXiv:1706.02808 [stat.CO].

- pdf(x)

ABSTRACT METHOD to evaluate pdf of distribution the samples mimic at locations of x.

IID Standard Uniform

- class qmcpy.discrete_distribution.iid_std_uniform.IIDStdUniform(dimension=1, seed=None)

A wrapper around NumPy’s IID Standard Uniform generator numpy.random.rand.

>>> dd = IIDStdUniform(dimension=2,seed=7) >>> dd.gen_samples(4) array([[0.04386058, 0.58727432], [0.3691824 , 0.65212985], [0.69669968, 0.10605352], [0.63025643, 0.13630282]]) >>> dd IIDStdUniform (DiscreteDistribution Object) d 2^(1) entropy 7 spawn_key ()

- __init__(dimension=1, seed=None)

- gen_samples(n)

Generate samples

- Parameters

n (int) – Number of observations to generate

- Returns

n x self.d array of samples

- Return type

ndarray

- pdf(x)

ABSTRACT METHOD to evaluate pdf of distribution the samples mimic at locations of x.

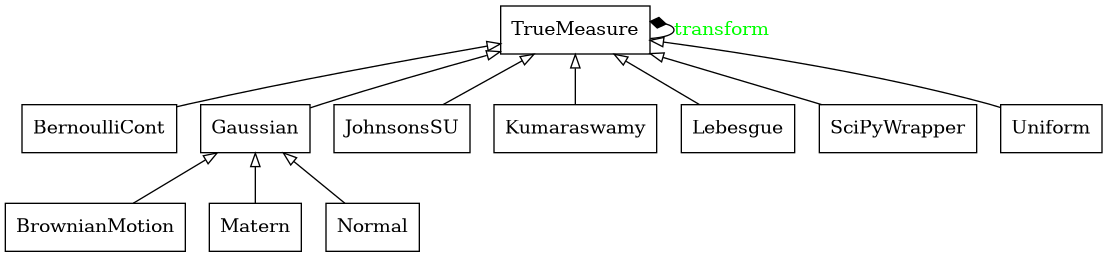

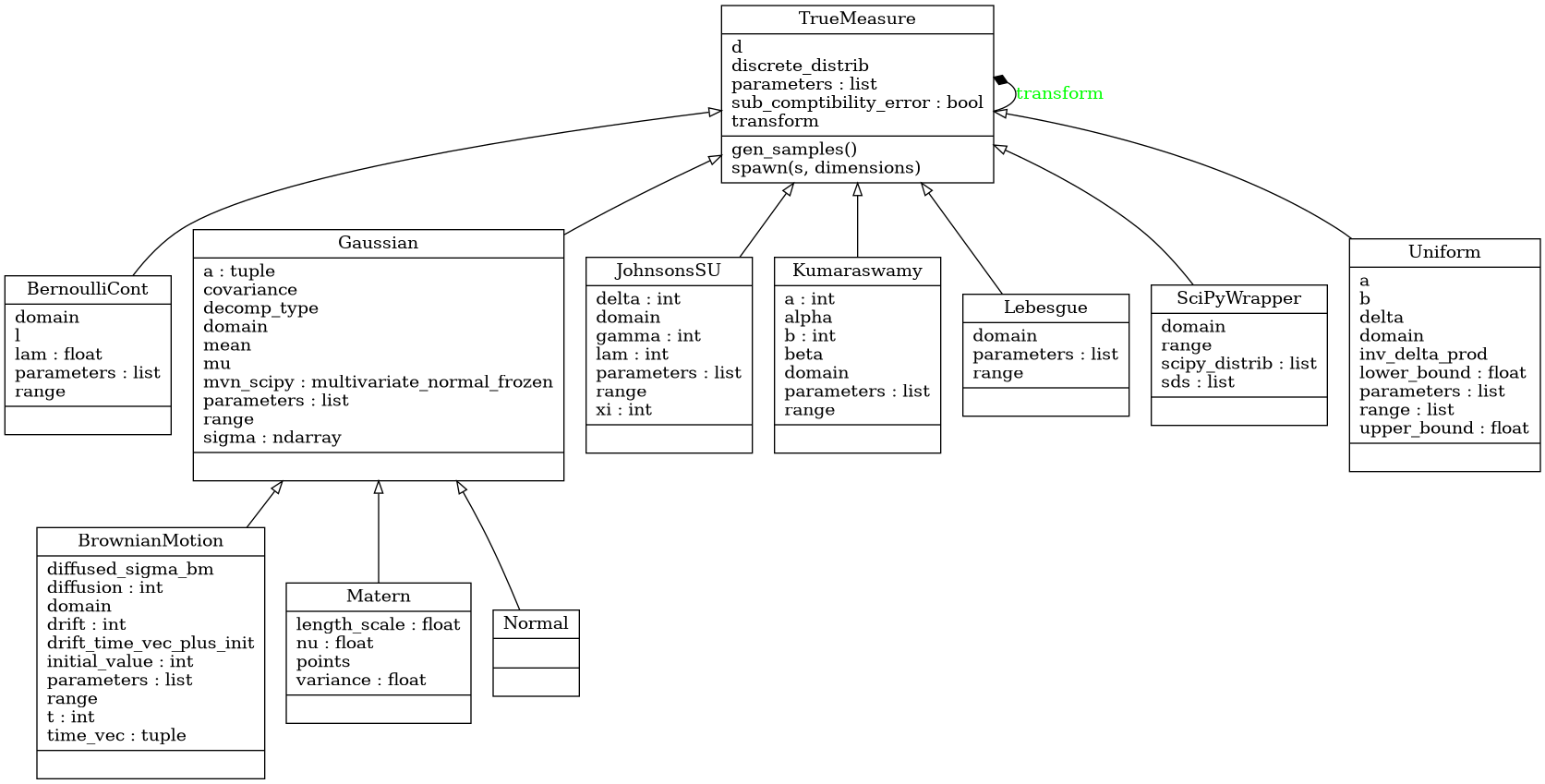

True Measure Class

Abstract Measure Class

- class qmcpy.true_measure._true_measure.TrueMeasure

True Measure abstract class. DO NOT INSTANTIATE.

- gen_samples(*args, **kwargs)

Generate samples from the discrete distribution and transform them via the transform method.

- spawn(s=1, dimensions=None)

Spawn new instances of the current discrete distribution but with new seeds and dimensions. Developed for multi-level and multi-replication (Q)MC algorithms.

Uniform

- class qmcpy.true_measure.uniform.Uniform(sampler, lower_bound=0.0, upper_bound=1.0)

>>> u = Uniform(DigitalNetB2(2,seed=7),lower_bound=[0,.5],upper_bound=[2,3]) >>> u.gen_samples(4) array([[1.12538017, 0.93444992], [0.693306 , 2.12676579], [1.64149095, 2.88726434], [0.20844522, 1.73645241]]) >>> u Uniform (TrueMeasure Object) lower_bound [0. 0.5] upper_bound [2 3]

Gaussian

- class qmcpy.true_measure.gaussian.Gaussian(sampler, mean=0.0, covariance=1.0, decomp_type='PCA')

Normal Measure.

>>> g = Gaussian(DigitalNetB2(2,seed=7),mean=[1,2],covariance=[[9,4],[4,5]]) >>> g.gen_samples(4) array([[-0.23979685, 2.98944192], [ 2.45994002, 2.17853622], [-0.22923897, -1.92667105], [ 4.6127697 , 4.25820377]]) >>> g Gaussian (TrueMeasure Object) mean [1 2] covariance [[9 4] [4 5]] decomp_type PCA

- __init__(sampler, mean=0.0, covariance=1.0, decomp_type='PCA')

- Parameters

sampler (DiscreteDistribution/TrueMeasure) – A discrete distribution from which to transform samples or a true measure by which to compose a transform

mean (float) – mu for Normal(mu,sigma^2)

covariance (ndarray) – sigma^2 for Normal(mu,sigma^2). A float or d (dimension) vector input will be extended to covariance*eye(d)

decomp_type (str) – method of decomposition either “PCA” for principal component analysis or “Cholesky” for cholesky decomposition.

- class qmcpy.true_measure.gaussian.Normal(sampler, mean=0.0, covariance=1.0, decomp_type='PCA')

Brownian Motion

- class qmcpy.true_measure.brownian_motion.BrownianMotion(sampler, t_final=1, initial_value=0, drift=0, diffusion=1, decomp_type='PCA')

Geometric Brownian Motion.

>>> bm = BrownianMotion(DigitalNetB2(4,seed=7),t_final=2,drift=2) >>> bm.gen_samples(2) array([[0.44018403, 1.62690477, 2.69418273, 4.21753174], [1.97549563, 2.27002956, 2.92802765, 4.77126959]]) >>> bm BrownianMotion (TrueMeasure Object) time_vec [0.5 1. 1.5 2. ] drift 2^(1) mean [1. 2. 3. 4.] covariance [[0.5 0.5 0.5 0.5] [0.5 1. 1. 1. ] [0.5 1. 1.5 1.5] [0.5 1. 1.5 2. ]] decomp_type PCA

- __init__(sampler, t_final=1, initial_value=0, drift=0, diffusion=1, decomp_type='PCA')

BrowianMotion(t) = (initial_value) + (drift)*t + sqrt{diffusion}*StandardBrownianMotion(t)

- Parameters

sampler (DiscreteDistribution/TrueMeasure) – A discrete distribution from which to transform samples or a true measure by which to compose a transform

t_final (float) – end time for the Brownian Motion.

initial_value (float) – See above formula

drift (int) – See above formula

diffusion (int) – See above formula

decomp_type (str) – method of decomposition either “PCA” for principal component analysis or “Cholesky” for cholesky decomposition.

Lebesgue

- class qmcpy.true_measure.lebesgue.Lebesgue(sampler)

>>> Lebesgue(Gaussian(DigitalNetB2(2,seed=7))) Lebesgue (TrueMeasure Object) transform Gaussian (TrueMeasure Object) mean 0 covariance 1 decomp_type PCA >>> Lebesgue(Uniform(DigitalNetB2(2,seed=7))) Lebesgue (TrueMeasure Object) transform Uniform (TrueMeasure Object) lower_bound 0 upper_bound 1

- __init__(sampler)

- Parameters

sampler (TrueMeasure) – A true measure by which to compose a transform.

Continuous Bernoulli

- class qmcpy.true_measure.bernoulli_cont.BernoulliCont(sampler, lam=0.5)

>>> bc = BernoulliCont(DigitalNetB2(2,seed=7),lam=.2) >>> bc.gen_samples(4) array([[0.39545122, 0.10073414], [0.21719142, 0.48293404], [0.68958314, 0.90847415], [0.05871131, 0.33436033]]) >>> bc BernoulliCont (TrueMeasure Object) lam 0.200

See https://en.wikipedia.org/wiki/Continuous_Bernoulli_distribution

- __init__(sampler, lam=0.5)

- Parameters

sampler (DiscreteDistribution/TrueMeasure) – A discrete distribution from which to transform samples or a true measure by which to compose a transform

lam (ndarray) – 0 < lambda < 1, a shape parameter, independent for each dimension

Johnson’s SU

- class qmcpy.true_measure.johnsons_su.JohnsonsSU(sampler, gamma=1, xi=1, delta=2, lam=2)

>>> jsu = JohnsonsSU(DigitalNetB2(2,seed=7),gamma=1,xi=2,delta=3,lam=4) >>> jsu.gen_samples(4) array([[ 0.86224892, -0.76967276], [ 0.07317047, 1.17727769], [ 1.89093286, 2.9341619 ], [-1.30283298, 0.62269632]]) >>> jsu JohnsonsSU (TrueMeasure Object) gamma 1 xi 2^(1) delta 3 lam 2^(2)

See https://en.wikipedia.org/wiki/Johnson%27s_SU-distribution

- __init__(sampler, gamma=1, xi=1, delta=2, lam=2)

- Parameters

sampler (DiscreteDistribution/TrueMeasure) – A discrete distribution from which to transform samples or a true measure by which to compose a transform

gamma (ndarray) – gamma

xi (ndarray) – xi

delta (ndarray) – delta > 0

lam (ndarray) – lambda > 0

Kumaraswamy

- class qmcpy.true_measure.kumaraswamy.Kumaraswamy(sampler, a=2, b=2)

>>> k = Kumaraswamy(DigitalNetB2(2,seed=7),a=[1,2],b=[3,4]) >>> k.gen_samples(4) array([[0.24096272, 0.21587652], [0.13227662, 0.4808615 ], [0.43615893, 0.73428949], [0.03602294, 0.39602319]]) >>> k Kumaraswamy (TrueMeasure Object) a [1 2] b [3 4]

See https://en.wikipedia.org/wiki/Kumaraswamy_distribution

- __init__(sampler, a=2, b=2)

- Parameters

sampler (DiscreteDistribution/TrueMeasure) – A discrete distribution from which to transform samples or a true measure by which to compose a transform

a (ndarray) – alpha > 0

b (ndarray) – beta > 0

SciPy Wrapper

- class qmcpy.true_measure.scipy_wrapper.SciPyWrapper(discrete_distrib, scipy_distribs)

Multivariate True Measure from Independent SciPy 1 Dimensional Marginals

>>> unif_gauss_gamma = SciPyWrapper( ... discrete_distrib = DigitalNetB2(3,seed=7), ... scipy_distribs = [ ... scipy.stats.uniform(loc=1,scale=2), ... scipy.stats.norm(loc=3,scale=4), ... scipy.stats.gamma(a=5,loc=6,scale=7)]) >>> unif_gauss_gamma.range array([[ 1., 3.], [-inf, inf], [ 6., inf]]) >>> unif_gauss_gamma.gen_samples(4) array([[ 2.12538017, -0.75733093, 38.28471046], [ 1.693306 , 4.54891231, 80.23287215], [ 2.64149095, 9.77761625, 43.6883765 ], [ 1.20844522, 2.94566431, 22.68122716]]) >>> betas_2d = SciPyWrapper(discrete_distrib=DigitalNetB2(2,seed=7),scipy_distribs=scipy.stats.beta(a=5,b=1)) >>> betas_2d.gen_samples(4) array([[0.89136146, 0.70469298], [0.80905676, 0.91764986], [0.96126183, 0.99081392], [0.63619813, 0.86865531]])

- __init__(discrete_distrib, scipy_distribs)

- Parameters

sampler (DiscreteDistribution/TrueMeasure) – A discrete distribution from which to transform samples or a true measure by which to compose a transform

scipy_distribs (list) – instantiated CONTINUOUS UNIVARIATE scipy.stats distributions https://docs.scipy.org/doc/scipy/reference/stats.html#continuous-distributions

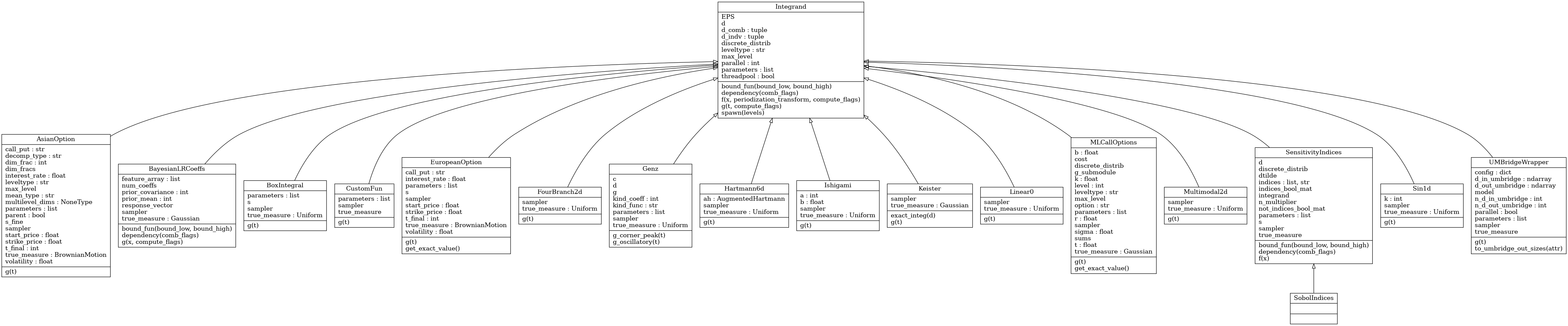

Integrand Class

Abstract Integrand Class

- class qmcpy.integrand._integrand.Integrand(dimension_indv, dimension_comb, parallel, threadpool=False)

Integrand abstract class. DO NOT INSTANTIATE.

- __init__(dimension_indv, dimension_comb, parallel, threadpool=False)

- Parameters

dimension_indv (tuple) – individual solution shape.

dimension_comb (tuple) – combined solution shape.

parallel (int) – If parallel is False, 0, or 1: function evaluation is done in serial fashion. Otherwise, parallel specifies the number of processes used by multiprocessing.Pool or multiprocessing.pool.ThreadPool. Passing parallel=True sets processes = os.cpu_count().

threadpool (bool) – When parallel > 1, if threadpool = True then use multiprocessing.pool.ThreadPool else use multiprocessing.Pool.

- bound_fun(bound_low, bound_high)

Compute the bounds on the combined function based on bounds for the individual functions. Defaults to the identity where we essentially do not combine integrands, but instead integrate each function individually.

- Parameters

bound_low (ndarray) – length Integrand.d_indv lower error bound

bound_high (ndarray) – length Integrand.d_indv upper error bound

- Returns

(tuple) containing

(ndarray): lower bound on function combining estimates

(ndarray): upper bound on function combining estimates

(ndarray): bool flags to override sufficient combined integrand estimation, e.g., when approximating a ratio of integrals, if the denominator’s bounds straddle 0, then returning True here forces ratio to be flagged as insufficiently approximated.

- dependency(comb_flags)

Takes a vector of indicators of weather of not the error bound is satisfied for combined integrands and which returns flags for individual integrands. For example, if we are taking the ratio of 2 individual integrands, then getting flag_comb=True means the ratio has not been approximated to within the tolerance, so the dependency function should return [True,True] indicating that both the numerator and denominator integrands need to be better approximated. :param comb_flags: flags indicating weather the combined integrals are insufficiently approximated :type comb_flags: bool ndarray

- Returns

length (Integrand.d_indv) flags for individual integrands

- Return type

(bool ndarray)

- f(x, periodization_transform='NONE', compute_flags=None, *args, **kwargs)

Evaluate transformed integrand based on true measures and discrete distribution

- Parameters

x (ndarray) – n x d array of samples from a discrete distribution

periodization_transform (str) – periodization transform

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

*args – other ordered args to g

**kwargs (dict) – other keyword args to g

- Returns

length n vector of function evaluations

- Return type

ndarray

- g(t, compute_flags=None, *args, **kwargs)

ABSTRACT METHOD for original integrand to be integrated.

- Parameters

t (ndarray) – n x d array of samples to be input into original integrand.

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

- Returns

n vector of function evaluations

- Return type

ndarray

Custom Function

- class qmcpy.integrand.custom_fun.CustomFun(true_measure, g, dimension_indv=1, parallel=False)

Integrand wrapper for a user’s function

>>> cf = CustomFun( ... true_measure = Gaussian(DigitalNetB2(2,seed=7),mean=[1,2]), ... g = lambda x: x[:,0]**2*x[:,1], ... dimension_indv = 1) >>> x = cf.discrete_distrib.gen_samples(2**10) >>> y = cf.f(x) >>> y.shape (1024, 1) >>> y.mean() 3.995... >>> cf = CustomFun( ... true_measure = Uniform(DigitalNetB2(3,seed=7),lower_bound=[2,3,4],upper_bound=[4,5,6]), ... g = lambda x,compute_flags=None: x, ... dimension_indv = 3) >>> x = cf.discrete_distrib.gen_samples(2**10) >>> y = cf.f(x) >>> y.shape (1024, 3) >>> y.mean(0) array([3., 4., 5.])

- __init__(true_measure, g, dimension_indv=1, parallel=False)

- Parameters

true_measure (TrueMeasure) – a TrueMeasure instance.

g (function) – a function handle.

dimension_indv (tuple) – individual solution dimensions.

parallel (int) – If parallel is False, 0, or 1: function evaluation is done in serial fashion. Otherwise, parallel specifies the number of CPUs used by multiprocessing.Pool. Passing parallel=True sets the number of CPUs equal to os.cpu_count(). Do NOT set g to a lambda function when doing parallel computation

- g(t, *args, **kwargs)

ABSTRACT METHOD for original integrand to be integrated.

- Parameters

t (ndarray) – n x d array of samples to be input into original integrand.

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

- Returns

n vector of function evaluations

- Return type

ndarray

Keister Function

- class qmcpy.integrand.keister.Keister(sampler)

.

.The standard example integrates the Keister integrand with respect to an IID Gaussian distribution with variance 1./2.

>>> k = Keister(DigitalNetB2(2,seed=7)) >>> x = k.discrete_distrib.gen_samples(2**10) >>> y = k.f(x) >>> y.mean() 1.808... >>> k.true_measure Gaussian (TrueMeasure Object) mean 0 covariance 2^(-1) decomp_type PCA >>> k = Keister(Gaussian(DigitalNetB2(2,seed=7),mean=0,covariance=2)) >>> x = k.discrete_distrib.gen_samples(2**12) >>> y = k.f(x) >>> y.mean() 1.808... >>> yp = k.f(x,periodization_transform='c2sin') >>> yp.mean() 1.807...

References

[1] B. D. Keister, Multidimensional Quadrature Algorithms, Computers in Physics, 10, pp. 119-122, 1996.

- __init__(sampler)

- Parameters

sampler (DiscreteDistribution/TrueMeasure) – A discrete distribution from which to transform samples or a true measure by which to compose a transform

- exact_integ(d)

computes the true value of the Keister integral in dimension d. Accuracy might degrade as d increases due to round-off error. :param d: :return: true_integral

- g(t)

ABSTRACT METHOD for original integrand to be integrated.

- Parameters

t (ndarray) – n x d array of samples to be input into original integrand.

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

- Returns

n vector of function evaluations

- Return type

ndarray

Box Integral

- class qmcpy.integrand.box_integral.BoxIntegral(sampler, s=array([1, 2]))

>>> l1 = BoxIntegral(DigitalNetB2(2,seed=7), s=[7]) >>> x1 = l1.discrete_distrib.gen_samples(2**10) >>> y1 = l1.f(x1) >>> y1.shape (1024, 1) >>> y1.mean(0) array([0.75156724]) >>> l2 = BoxIntegral(DigitalNetB2(5,seed=7), s=[-7,7]) >>> x2 = l2.discrete_distrib.gen_samples(2**10) >>> y2 = l2.f(x2,compute_flags=[1,1]) >>> y2.shape (1024, 2) >>> y2.mean(0) array([ 6.67548708, 10.52267786])

References:

[1] D.H. Bailey, J.M. Borwein, R.E. Crandall,Box integrals, Journal of Computational and Applied Mathematics, Volume 206, Issue 1, 2007, Pages 196-208, ISSN 0377-0427, https://doi.org/10.1016/j.cam.2006.06.010. (https://www.sciencedirect.com/science/article/pii/S0377042706004250)

[2] https://www.davidhbailey.com/dhbpapers/boxintegrals.pdf

- __init__(sampler, s=array([1, 2]))

- Parameters

sampler (DiscreteDistribution/TrueMeasure) – A discrete distribution from which to transform samples or a true measure by which to compose a transform

s (list or ndarray) – vectorized s parameter, len(s) is the number of vectorized integrals to evaluate.

- g(t, **kwargs)

ABSTRACT METHOD for original integrand to be integrated.

- Parameters

t (ndarray) – n x d array of samples to be input into original integrand.

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

- Returns

n vector of function evaluations

- Return type

ndarray

European Option

- class qmcpy.integrand.european_option.EuropeanOption(sampler, volatility=0.5, start_price=30, strike_price=35, interest_rate=0, t_final=1, call_put='call')

European financial option.

>>> eo = EuropeanOption(DigitalNetB2(4,seed=7),call_put='put') >>> eo EuropeanOption (Integrand Object) volatility 2^(-1) call_put put start_price 30 strike_price 35 interest_rate 0 >>> x = eo.discrete_distrib.gen_samples(2**12) >>> y = eo.f(x) >>> y.mean() 9.209... >>> eo = EuropeanOption(BrownianMotion(DigitalNetB2(4,seed=7),drift=1),call_put='put') >>> x = eo.discrete_distrib.gen_samples(2**12) >>> y = eo.f(x) >>> y.mean() 9.162... >>> eo.get_exact_value() 9.211452976234058

- __init__(sampler, volatility=0.5, start_price=30, strike_price=35, interest_rate=0, t_final=1, call_put='call')

- Parameters

sampler (DiscreteDistribution/TrueMeasure) – A discrete distribution from which to transform samples or a true measure by which to compose a transform

volatility (float) – sigma, the volatility of the asset

start_price (float) – S(0), the asset value at t=0

strike_price (float) – strike_price, the call/put offer

interest_rate (float) – r, the annual interest rate

t_final (float) – exercise time

call_put (str) – ‘call’ or ‘put’ option

- g(t)

See abstract method.

Asian Option

- class qmcpy.integrand.asian_option.AsianOption(sampler, volatility=0.5, start_price=30.0, strike_price=35.0, interest_rate=0.0, t_final=1, call_put='call', mean_type='arithmetic', multilevel_dims=None, decomp_type='PCA', _dim_frac=0)

Asian financial option.

>>> ac = AsianOption(DigitalNetB2(4,seed=7)) >>> ac AsianOption (Integrand Object) volatility 2^(-1) call_put call start_price 30 strike_price 35 interest_rate 0 mean_type arithmetic dim_frac 0 >>> x = ac.discrete_distrib.gen_samples(2**12) >>> y = ac.f(x) >>> y.mean() 1.768... >>> level_dims = [2,4,8] >>> ac2_multilevel = AsianOption(DigitalNetB2(seed=7),multilevel_dims=level_dims) >>> levels_to_spawn = arange(ac2_multilevel.max_level+1) >>> ac2_single_levels = ac2_multilevel.spawn(levels_to_spawn) >>> yml = 0 >>> for ac2_single_level in ac2_single_levels: ... x = ac2_single_level.discrete_distrib.gen_samples(2**12) ... level_est = ac2_single_level.f(x).mean() ... yml += level_est >>> yml 1.779...

- __init__(sampler, volatility=0.5, start_price=30.0, strike_price=35.0, interest_rate=0.0, t_final=1, call_put='call', mean_type='arithmetic', multilevel_dims=None, decomp_type='PCA', _dim_frac=0)

- Parameters

sampler (DiscreteDistribution/TrueMeasure) – A discrete distribution from which to transform samples or a true measure by which to compose a transform

volatility (float) – sigma, the volatility of the asset

start_price (float) – S(0), the asset value at t=0

strike_price (float) – strike_price, the call/put offer

interest_rate (float) – r, the annual interest rate

t_final (float) – exercise time

mean_type (string) – ‘arithmetic’ or ‘geometric’ mean

multilevel_dims (list of ints) – list of dimensions at each level. Leave as None for single-level problems

_dim_frac (float) – for internal use only, users should not set this parameter.

- g(t)

ABSTRACT METHOD for original integrand to be integrated.

- Parameters

t (ndarray) – n x d array of samples to be input into original integrand.

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

- Returns

n vector of function evaluations

- Return type

ndarray

Multilevel Call Options with Milstein Discretization

- class qmcpy.integrand.ml_call_options.MLCallOptions(sampler, option='european', volatility=0.2, start_strike_price=100.0, interest_rate=0.05, t_final=1.0, _level=0)

Various call options from finance using Milstein discretization with

timesteps on level

timesteps on level  .

.>>> mlco_original = MLCallOptions(DigitalNetB2(seed=7)) >>> mlco_original MLCallOptions (Integrand Object) option european sigma 0.200 k 100 r 0.050 t 1 b 85 level 0 >>> mlco_ml_dims = mlco_original.spawn(levels=arange(4)) >>> yml = 0 >>> for mlco in mlco_ml_dims: ... x = mlco.discrete_distrib.gen_samples(2**10) ... yml += mlco.f(x).mean() >>> yml 10.393...

References:

[1] M.B. Giles. Improved multilevel Monte Carlo convergence using the Milstein scheme. 343-358, in Monte Carlo and Quasi-Monte Carlo Methods 2006, Springer, 2008. http://people.maths.ox.ac.uk/~gilesm/files/mcqmc06.pdf.

- __init__(sampler, option='european', volatility=0.2, start_strike_price=100.0, interest_rate=0.05, t_final=1.0, _level=0)

- Parameters

sampler (DiscreteDistribution/TrueMeasure) – A discrete distribution from which to transform samples or a true measure by which to compose a transform

option_type (str) – type of option in [“European”,”Asian”]

volatility (float) – sigma, the volatility of the asset

start_strike_price (float) – S(0), the asset value at t=0, and K, the strike price. Assume start_price = strike_price

interest_rate (float) – r, the annual interest rate

t_final (float) – exercise time

_level (int) – for internal use only, users should not set this parameter.

- g(t)

- Parameters

t (ndarray) – Gaussian(0,1^2) samples

- Returns

First, an ndarray of length 6 vector of summary statistic sums. Second, a float of cost on this level.

- Return type

- get_exact_value()

Print exact analytic value, based on s0=k.

Linear Function

- class qmcpy.integrand.linear0.Linear0(sampler)

>>> l = Linear0(DigitalNetB2(100,seed=7)) >>> x = l.discrete_distrib.gen_samples(2**10) >>> y = l.f(x) >>> y.mean() -1.175...e-08 >>> ytf = l.f(x,periodization_transform='C1SIN') >>> ytf.mean() -4.050...e-12

- __init__(sampler)

- Parameters

sampler (DiscreteDistribution/TrueMeasure) – A discrete distribution from which to transform samples or a true measure by which to compose a transform

- g(t)

ABSTRACT METHOD for original integrand to be integrated.

- Parameters

t (ndarray) – n x d array of samples to be input into original integrand.

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

- Returns

n vector of function evaluations

- Return type

ndarray

Bayesian Logistic Regression

- class qmcpy.integrand.bayesian_lr_coeffs.BayesianLRCoeffs(sampler, feature_array, response_vector, prior_mean=0, prior_covariance=10)

Logistic Regression Coefficients computed as the posterior mean in a Bayesian framework.

>>> blrcoeffs = BayesianLRCoeffs(DigitalNetB2(3,seed=7),feature_array=arange(8).reshape((4,2)),response_vector=[0,0,1,1]) >>> x = blrcoeffs.discrete_distrib.gen_samples(2**10) >>> y = blrcoeffs.f(x) >>> y.shape (1024, 2, 3) >>> y.mean(0) array([[ 0.04639394, -0.01440543, -0.05498496], [ 0.02176581, 0.02176581, 0.02176581]])

- __init__(sampler, feature_array, response_vector, prior_mean=0, prior_covariance=10)

- Parameters

sampler (DiscreteDistribution/TrueMeasure) – A discrete distribution from which to transform samples or a true measure by which to compose a transform

feature_array (ndarray) – N samples by d-1 dimensions array of input features

response_vector (ndarray) – length N array of binary responses corresponding to each

prior_mean (ndarray) – length d array of prior means, one for each coefficient. The first d-1 inputs correspond to the d-1 features. The last input corresponds to the intercept coefficient.

prior_covariance (ndarray) – d x d prior covariance array whose indexing is consistent with the prior mean.

- bound_fun(bound_low, bound_high)

Compute the bounds on the combined function based on bounds for the individual functions. Defaults to the identity where we essentially do not combine integrands, but instead integrate each function individually.

- Parameters

bound_low (ndarray) – length Integrand.d_indv lower error bound

bound_high (ndarray) – length Integrand.d_indv upper error bound

- Returns

(tuple) containing

(ndarray): lower bound on function combining estimates

(ndarray): upper bound on function combining estimates

(ndarray): bool flags to override sufficient combined integrand estimation, e.g., when approximating a ratio of integrals, if the denominator’s bounds straddle 0, then returning True here forces ratio to be flagged as insufficiently approximated.

- dependency(comb_flags)

Takes a vector of indicators of weather of not the error bound is satisfied for combined integrands and which returns flags for individual integrands. For example, if we are taking the ratio of 2 individual integrands, then getting flag_comb=True means the ratio has not been approximated to within the tolerance, so the dependency function should return [True,True] indicating that both the numerator and denominator integrands need to be better approximated. :param comb_flags: flags indicating weather the combined integrals are insufficiently approximated :type comb_flags: bool ndarray

- Returns

length (Integrand.d_indv) flags for individual integrands

- Return type

(bool ndarray)

- g(x, compute_flags)

ABSTRACT METHOD for original integrand to be integrated.

- Parameters

t (ndarray) – n x d array of samples to be input into original integrand.

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

- Returns

n vector of function evaluations

- Return type

ndarray

Genz Function

- class qmcpy.integrand.genz.Genz(sampler, kind_func='oscilatory', kind_coeff=1)

-

>>> for kind_func in ['oscilatory','corner-peak']: ... for kind_coeff in [1,2,3]: ... g = Genz(DigitalNetB2(2,seed=7),kind_func=kind_func,kind_coeff=kind_coeff) ... x = g.discrete_distrib.gen_samples(2**14) ... y = g.f(x) ... mu_hat = y.mean() ... print('%-15s %-3d %.3f'%(kind_func,kind_coeff,mu_hat)) oscilatory 1 -0.351 oscilatory 2 -0.380 oscilatory 3 -0.217 corner-peak 1 0.713 corner-peak 2 0.712 corner-peak 3 0.720

- __init__(sampler, kind_func='oscilatory', kind_coeff=1)

Ishigami Function

- class qmcpy.integrand.ishigami.Ishigami(sampler, a=7, b=0.1)

https://www.sfu.ca/~ssurjano/ishigami.html

>>> ishigami = Ishigami(DigitalNetB2(3,seed=7)) >>> x = ishigami.discrete_distrib.gen_samples(2**10) >>> y = ishigami.f(x) >>> y.mean() 3.499... >>> ishigami.true_measure Uniform (TrueMeasure Object) lower_bound -3.142 upper_bound 3.142

- References

[1] Ishigami, T., & Homma, T. (1990, December). An importance quantification technique in uncertainty analysis for computer models. In Uncertainty Modeling and Analysis, 1990. Proceedings., First International Symposium on (pp. 398-403). IEEE.

- __init__(sampler, a=7, b=0.1)

- g(t)

ABSTRACT METHOD for original integrand to be integrated.

- Parameters

t (ndarray) – n x d array of samples to be input into original integrand.

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

- Returns

n vector of function evaluations

- Return type

ndarray

Sensitivity Indices

- class qmcpy.integrand.sensitivity_indices.SensitivityIndices(integrand, indices='singletons')

Sensitivity’ Indicies, normalized Sobol’ Indices.

>>> dnb2 = DigitalNetB2(dimension=3,seed=7) >>> keister_d = Keister(dnb2) >>> keister_indices = SensitivityIndices(keister_d,indices='singletons') >>> sc = CubQMCNetG(keister_indices,abs_tol=1e-3) >>> solution,data = sc.integrate() >>> solution.squeeze() array([[0.32803639, 0.32795358, 0.32807359], [0.33884667, 0.33857811, 0.33884115]]) >>> data LDTransformData (AccumulateData Object) solution [[0.328 0.328 0.328] [0.339 0.339 0.339]] comb_bound_low [[0.327 0.327 0.328] [0.338 0.338 0.338]] comb_bound_high [[0.329 0.329 0.329] [0.34 0.339 0.34 ]] comb_flags [[ True True True] [ True True True]] n_total 2^(16) n [[[65536. 65536. 65536.] [65536. 65536. 65536.] [65536. 65536. 65536.]] [[32768. 32768. 32768.] [32768. 32768. 32768.] [32768. 32768. 32768.]]] time_integrate ... CubQMCNetG (StoppingCriterion Object) abs_tol 0.001 rel_tol 0 n_init 2^(10) n_max 2^(35) SensitivityIndices (Integrand Object) indices [[0] [1] [2]] n_multiplier 3 Gaussian (TrueMeasure Object) mean 0 covariance 2^(-1) decomp_type PCA DigitalNetB2 (DiscreteDistribution Object) d 6 dvec [0 1 2 3 4 5] randomize LMS_DS graycode 0 entropy 7 spawn_key (0,) >>> sc = CubQMCNetG(SobolIndices(BoxIntegral(DigitalNetB2(3,seed=7)),indices='all'),abs_tol=.01) >>> sol,data = sc.integrate() >>> print(sol) [[[0.32312991 0.33340559] [0.32331463 0.33342669] [0.32160276 0.33318619] [0.65559598 0.6667154 ] [0.65551702 0.66670251] [0.6556618 0.66672429]] [[0.3440018 0.33341845] [0.34501082 0.33347005] [0.34504829 0.33345212] [0.67659368 0.6667021 ] [0.67725088 0.66667925] [0.67802866 0.66672587]]]

References

[1] Art B. Owen.Monte Carlo theory, methods and examples. 2013. Appendix A.

- __init__(integrand, indices='singletons')

- Parameters

integrand (Integrand) – integrand to find Sobol’ indices of

indices (list of lists) – each element of indices should be a list of indices, u, at which to compute the Sobol’ indices. The default indices=’singletons’ sets indices=[[0],[1],…[d-1]]. Should not include [], the null set, or [0,…,d-1], the set of all indices. Setting indices=’all’ will compute all sensitivity indices

- bound_fun(bound_low, bound_high)

Compute the bounds on the combined function based on bounds for the individual functions. Defaults to the identity where we essentially do not combine integrands, but instead integrate each function individually.

- Parameters

bound_low (ndarray) – length Integrand.d_indv lower error bound

bound_high (ndarray) – length Integrand.d_indv upper error bound

- Returns

(tuple) containing

(ndarray): lower bound on function combining estimates

(ndarray): upper bound on function combining estimates

(ndarray): bool flags to override sufficient combined integrand estimation, e.g., when approximating a ratio of integrals, if the denominator’s bounds straddle 0, then returning True here forces ratio to be flagged as insufficiently approximated.

- dependency(comb_flags)

Takes a vector of indicators of weather of not the error bound is satisfied for combined integrands and which returns flags for individual integrands. For example, if we are taking the ratio of 2 individual integrands, then getting flag_comb=True means the ratio has not been approximated to within the tolerance, so the dependency function should return [True,True] indicating that both the numerator and denominator integrands need to be better approximated. :param comb_flags: flags indicating weather the combined integrals are insufficiently approximated :type comb_flags: bool ndarray

- Returns

length (Integrand.d_indv) flags for individual integrands

- Return type

(bool ndarray)

- f(x, *args, **kwargs)

Evaluate transformed integrand based on true measures and discrete distribution

- Parameters

x (ndarray) – n x d array of samples from a discrete distribution

periodization_transform (str) – periodization transform

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

*args – other ordered args to g

**kwargs (dict) – other keyword args to g

- Returns

length n vector of function evaluations

- Return type

ndarray

- class qmcpy.integrand.sensitivity_indices.SobolIndices(integrand, indices='singletons')

Normalized Sobol’ Indices, an alias for SensitivityIndices.

UM-Bridge Wrapper

- class qmcpy.integrand.um_bridge_wrapper.UMBridgeWrapper(true_measure, model, config={}, parallel=False)

UM-Bridge Model Wrapper. Requires Docker be installed, see https://www.docker.com/.

>>> _ = os.system('docker run --name muqbp -dit -p 4243:4243 linusseelinger/benchmark-muq-beam-propagation:latest > /dev/null') >>> import umbridge >>> dnb2 = DigitalNetB2(dimension=3,seed=7) >>> distribution = Uniform(dnb2,lower_bound=1,upper_bound=1.05) >>> model = umbridge.HTTPModel('http://localhost:4243','forward') >>> umbridge_config = {"d": dnb2.d} >>> um_bridge_integrand = UMBridgeWrapper(distribution,model,umbridge_config,parallel=False) >>> solution,data = CubQMCNetG(um_bridge_integrand,abs_tol=5e-2).integrate() >>> print(data) LDTransformData (AccumulateData Object) solution [ 0. 3.855 14.69 ... 898.921 935.383 971.884] comb_bound_low [ 0. 3.854 14.688 ... 898.901 935.363 971.863] comb_bound_high [ 0. 3.855 14.691 ... 898.941 935.404 971.906] comb_flags [ True True True ... True True True] n_total 2^(11) n [1024. 1024. 1024. ... 2048. 2048. 2048.] time_integrate ... CubQMCNetG (StoppingCriterion Object) abs_tol 0.050 rel_tol 0 n_init 2^(10) n_max 2^(35) UMBridgeWrapper (Integrand Object) Uniform (TrueMeasure Object) lower_bound 1 upper_bound 1.050 DigitalNetB2 (DiscreteDistribution Object) d 3 dvec [0 1 2] randomize LMS_DS graycode 0 entropy 7 spawn_key () >>> _ = os.system('docker rm -f muqbp > /dev/null') >>> class TestModel(umbridge.Model): ... def __init__(self): ... super().__init__("forward") ... def get_input_sizes(self, config): ... return [1,2,3] ... def get_output_sizes(self, config): ... return [3,2,1] ... def __call__(self, parameters, config): ... out0 = [parameters[2][0],sum(parameters[2][:2]),sum(parameters[2])] ... out1 = [parameters[1][0],sum(parameters[1])] ... out2 = [parameters[0]] ... return [out0,out1,out2] ... def supports_evaluate(self): ... return True >>> my_model = TestModel() >>> my_distribution = Uniform( ... sampler = DigitalNetB2(dimension=sum(my_model.get_input_sizes(config={})),seed=7), ... lower_bound = -1, ... upper_bound = 1) >>> my_integrand = UMBridgeWrapper(my_distribution,my_model) >>> my_solution,my_data = CubQMCNetG(my_integrand,abs_tol=5e-2).integrate() >>> my_data LDTransformData (AccumulateData Object) solution [-2.328e-10 -4.657e-10 -6.985e-10 -2.328e-10 -4.657e-10 -2.328e-10] comb_bound_low [-9.649e-06 -1.765e-04 -2.352e-04 -3.053e-07 -1.997e-05 -1.952e-05] comb_bound_high [9.649e-06 1.765e-04 2.352e-04 3.048e-07 1.997e-05 1.952e-05] comb_flags [ True True True True True True] n_total 2^(10) n [1024. 1024. 1024. 1024. 1024. 1024.] time_integrate ... CubQMCNetG (StoppingCriterion Object) abs_tol 0.050 rel_tol 0 n_init 2^(10) n_max 2^(35) UMBridgeWrapper (Integrand Object) Uniform (TrueMeasure Object) lower_bound -1 upper_bound 1 DigitalNetB2 (DiscreteDistribution Object) d 6 dvec [0 1 2 3 4 5] randomize LMS_DS graycode 0 entropy 7 spawn_key () >>> my_integrand.to_umbridge_out_sizes(my_solution) [[-2.3283064365386963e-10, -4.656612873077393e-10, -6.984919309616089e-10], [-2.3283064365386963e-10, -4.656612873077393e-10], [-2.3283064365386963e-10]] >>> my_integrand.to_umbridge_out_sizes(my_data.comb_bound_low) [[-9.649316780269146e-06, -0.00017654551993473433, -0.00023524149401055183], [-3.0527962735504843e-07, -1.997367189687793e-05], [-1.9521190552040935e-05]] >>> my_integrand.to_umbridge_out_sizes(my_data.comb_bound_high) [[9.648851118981838e-06, 0.00017654458861215971, 0.0002352400970266899], [3.048139660677407e-07, 1.9972740574303316e-05], [1.9520724890753627e-05]]

References

[1] UM-Bridge documentation. https://um-bridge-benchmarks.readthedocs.io/en/docs/index.html

- __init__(true_measure, model, config={}, parallel=False)

See https://um-bridge-benchmarks.readthedocs.io/en/docs/umbridge/clients.html

- Parameters

true_measure (TrueMeasure) – a TrueMeasure instance.

model (umbridge.HTTPModel) – a UM-Bridge model

config (dict) – config keyword argument to umbridge.HTTPModel(url,name).__call__

parallel (int) – If parallel is False, 0, or 1: function evaluation is done in serial fashion. Otherwise, parallel specifies the number of processes used by multiprocessing.Pool or multiprocessing.pool.ThreadPool. Passing parallel=True sets processes = os.cpu_count().

- g(t, **kwargs)

ABSTRACT METHOD for original integrand to be integrated.

- Parameters

t (ndarray) – n x d array of samples to be input into original integrand.

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

- Returns

n vector of function evaluations

- Return type

ndarray

Sin 1d

- class qmcpy.integrand.sin1d.Sin1d(sampler, k=1)

>>> sin1d = Sin1d(DigitalNetB2(1,seed=7)) >>> x = sin1d.discrete_distrib.gen_samples(2**10) >>> y = sin1d.f(x) >>> y.mean() 7.33449186...e-08 >>> sin1d.true_measure Uniform (TrueMeasure Object) lower_bound 0 upper_bound 6.283

- g(t)

ABSTRACT METHOD for original integrand to be integrated.

- Parameters

t (ndarray) – n x d array of samples to be input into original integrand.

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

- Returns

n vector of function evaluations

- Return type

ndarray

Multimodal 2d

- class qmcpy.integrand.multimodal2d.Multimodal2d(sampler)

>>> mm2d = Multimodal2d(DigitalNetB2(2,seed=7)) >>> x = mm2d.discrete_distrib.gen_samples(2**10) >>> y = mm2d.f(x) >>> y.mean() -0.7365118306607449 >>> mm2d.true_measure Uniform (TrueMeasure Object) lower_bound [-4 -3] upper_bound [7 8]

- g(t)

ABSTRACT METHOD for original integrand to be integrated.

- Parameters

t (ndarray) – n x d array of samples to be input into original integrand.

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

- Returns

n vector of function evaluations

- Return type

ndarray

Four Branch 2d

- class qmcpy.integrand.fourbranch2d.FourBranch2d(sampler)

>>> fb2d = FourBranch2d(DigitalNetB2(2,seed=7)) >>> x = fb2d.discrete_distrib.gen_samples(2**10) >>> y = fb2d.f(x) >>> y.mean() -2.5003746135324247 >>> fb2d.true_measure Uniform (TrueMeasure Object) lower_bound -8 upper_bound 2^(3)

- g(t)

ABSTRACT METHOD for original integrand to be integrated.

- Parameters

t (ndarray) – n x d array of samples to be input into original integrand.

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

- Returns

n vector of function evaluations

- Return type

ndarray

Hartmann 6d

- class qmcpy.integrand.hartmann6d.Hartmann6d(sampler)

>>> h6d = Hartmann6d(DigitalNetB2(6,seed=7)) >>> x = h6d.discrete_distrib.gen_samples(2**10) >>> y = h6d.f(x) >>> y.mean() -0.2613140309713834 >>> h6d.true_measure Uniform (TrueMeasure Object) lower_bound 0 upper_bound 1

- g(t)

ABSTRACT METHOD for original integrand to be integrated.

- Parameters

t (ndarray) – n x d array of samples to be input into original integrand.

compute_flags (ndarray) – outputs that require computation. For example, if the vector function has 3 outputs and compute_flags = [False, True, False], then the function is only required to compute the second output and may leave the remaining outputs as e.g. 0. The False outputs will not be used in the computation since those integrals have been sufficiently approximated.

- Returns

n vector of function evaluations

- Return type

ndarray

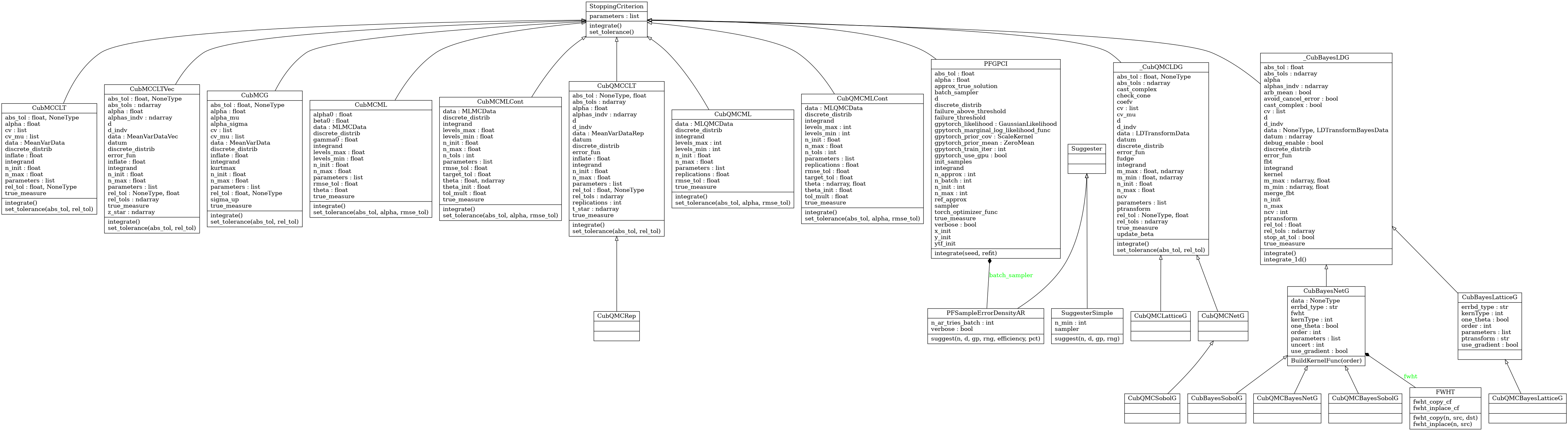

Stopping Criterion Algorithms

Abstract Stopping Criterion Class

- class qmcpy.stopping_criterion._stopping_criterion.StoppingCriterion(allowed_levels, allowed_distribs, allow_vectorized_integrals)

Stopping Criterion abstract class. DO NOT INSTANTIATE.

- __init__(allowed_levels, allowed_distribs, allow_vectorized_integrals)

- Parameters

distribution (DiscreteDistribution) – a DiscreteDistribution

allowed_levels (list) – which integrand types are supported: ‘single’, ‘fixed-multi’, ‘adaptive-multi’

allowed_distribs (list) – list of compatible DiscreteDistribution classes

- integrate()

ABSTRACT METHOD to determine the number of samples needed to satisfy the tolerance.

- Returns

- tuple containing:

solution (float): approximation to the integral

data (AccumulateData): an AccumulateData object

- Return type

- set_tolerance(*args, **kwargs)

ABSTRACT METHOD to reset the absolute tolerance.

Guaranteed Digital Net Cubature (QMC)

- class qmcpy.stopping_criterion.cub_qmc_net_g.CubQMCNetG(integrand, abs_tol=0.01, rel_tol=0.0, n_init=1024.0, n_max=34359738368.0, fudge=<function CubQMCNetG.<lambda>>, check_cone=False, control_variates=[], control_variate_means=[], update_beta=False, error_fun=<function CubQMCNetG.<lambda>>)

Quasi-Monte Carlo method using Sobol’ cubature over the d-dimensional region to integrate within a specified generalized error tolerance with guarantees under Walsh-Fourier coefficients cone decay assumptions.

>>> k = Keister(DigitalNetB2(2,seed=7)) >>> sc = CubQMCNetG(k,abs_tol=.05) >>> solution,data = sc.integrate() >>> data LDTransformData (AccumulateData Object) solution 1.809 comb_bound_low 1.804 comb_bound_high 1.814 comb_flags 1 n_total 2^(10) n 2^(10) time_integrate ... CubQMCNetG (StoppingCriterion Object) abs_tol 0.050 rel_tol 0 n_init 2^(10) n_max 2^(35) Keister (Integrand Object) Gaussian (TrueMeasure Object) mean 0 covariance 2^(-1) decomp_type PCA DigitalNetB2 (DiscreteDistribution Object) d 2^(1) dvec [0 1] randomize LMS_DS graycode 0 entropy 7 spawn_key () >>> dd = DigitalNetB2(3,seed=7) >>> g1 = CustomFun(Uniform(dd,0,2),lambda t: 10*t[:,0]-5*t[:,1]**2+t[:,2]**3) >>> cv1 = CustomFun(Uniform(dd,0,2),lambda t: t[:,0]) >>> cv2 = CustomFun(Uniform(dd,0,2),lambda t: t[:,1]**2) >>> sc = CubQMCNetG(g1,abs_tol=1e-6,check_cone=True, ... control_variates = [cv1,cv2], ... control_variate_means = [1,4/3]) >>> sol,data = sc.integrate() >>> sol array([5.33333333]) >>> exactsol = 16/3 >>> abs(sol-exactsol)<1e-6 array([ True]) >>> dnb2 = DigitalNetB2(3,seed=7) >>> f = BoxIntegral(dnb2, s=[-1,1]) >>> abs_tol = 1e-3 >>> sc = CubQMCNetG(f, abs_tol=abs_tol) >>> solution,data = sc.integrate() >>> solution array([1.18944142, 0.96064165]) >>> sol3neg1 = -pi/4-1/2*log(2)+log(5+3*sqrt(3)) >>> sol31 = sqrt(3)/4+1/2*log(2+sqrt(3))-pi/24 >>> true_value = array([sol3neg1,sol31]) >>> (abs(true_value-solution)<abs_tol).all() True >>> f2 = BoxIntegral(dnb2,s=[3,4]) >>> sc = CubQMCNetG(f2,control_variates=f,control_variate_means=true_value,update_beta=True) >>> solution,data = sc.integrate() >>> solution array([1.10168119, 1.26661293]) >>> data LDTransformData (AccumulateData Object) solution [1.102 1.267] comb_bound_low [1.099 1.262] comb_bound_high [1.104 1.271] comb_flags [ True True] n_total 2^(10) n [1024. 1024.] time_integrate ... CubQMCNetG (StoppingCriterion Object) abs_tol 0.010 rel_tol 0 n_init 2^(10) n_max 2^(35) cv BoxIntegral (Integrand Object) s [-1 1] cv_mu [1.19 0.961] update_beta 1 BoxIntegral (Integrand Object) s [3 4] Uniform (TrueMeasure Object) lower_bound 0 upper_bound 1 DigitalNetB2 (DiscreteDistribution Object) d 3 dvec [0 1 2] randomize LMS_DS graycode 0 entropy 7 spawn_key () >>> cf = CustomFun( ... true_measure = Uniform(DigitalNetB2(6,seed=7)), ... g = lambda x,compute_flags=None: (2*arange(1,7)*x).reshape(-1,2,3), ... dimension_indv = (2,3)) >>> sol,data = CubQMCNetG(cf,abs_tol=1e-6).integrate() >>> data LDTransformData (AccumulateData Object) solution [[1. 2. 3.] [4. 5. 6.]] comb_bound_low [[1. 2. 3.] [4. 5. 6.]] comb_bound_high [[1. 2. 3.] [4. 5. 6.]] comb_flags [[ True True True] [ True True True]] n_total 2^(13) n [[2048. 1024. 1024.] [8192. 4096. 2048.]] time_integrate ... CubQMCNetG (StoppingCriterion Object) abs_tol 1.00e-06 rel_tol 0 n_init 2^(10) n_max 2^(35) CustomFun (Integrand Object) Uniform (TrueMeasure Object) lower_bound 0 upper_bound 1 DigitalNetB2 (DiscreteDistribution Object) d 6 dvec [0 1 2 3 4 5] randomize LMS_DS graycode 0 entropy 7 spawn_key ()

Original Implementation:

References

[1] Fred J. Hickernell and Lluis Antoni Jimenez Rugama, Reliable adaptive cubature using digital sequences, 2014. Submitted for publication: arXiv:1410.8615.

[2] Sou-Cheng T. Choi, Yuhan Ding, Fred J. Hickernell, Lan Jiang, Lluis Antoni Jimenez Rugama, Da Li, Jagadeeswaran Rathinavel, Xin Tong, Kan Zhang, Yizhi Zhang, and Xuan Zhou, GAIL: Guaranteed Automatic Integration Library (Version 2.3) [MATLAB Software], 2019. Available from http://gailgithub.github.io/GAIL_Dev/

- Guarantee:

This algorithm computes the integral of real valued functions in

![[0,1]^d](_images/math/38fbdb5f0cd005023c1bb115f01c323f34f20446.png) with a prescribed generalized error tolerance. The Fourier coefficients

of the integrand are assumed to be absolutely convergent. If the

algorithm terminates without warning messages, the output is given with

guarantees under the assumption that the integrand lies inside a cone of

functions. The guarantee is based on the decay rate of the Fourier

coefficients. For integration over domains other than , this cone

condition applies to

with a prescribed generalized error tolerance. The Fourier coefficients

of the integrand are assumed to be absolutely convergent. If the

algorithm terminates without warning messages, the output is given with

guarantees under the assumption that the integrand lies inside a cone of

functions. The guarantee is based on the decay rate of the Fourier

coefficients. For integration over domains other than , this cone

condition applies to  (the composition of the

functions) where

(the composition of the

functions) where  is the transformation function for to

the desired region. For more details on how the cone is defined, please

refer to the references below.

is the transformation function for to

the desired region. For more details on how the cone is defined, please

refer to the references below.

- __init__(integrand, abs_tol=0.01, rel_tol=0.0, n_init=1024.0, n_max=34359738368.0, fudge=<function CubQMCNetG.<lambda>>, check_cone=False, control_variates=[], control_variate_means=[], update_beta=False, error_fun=<function CubQMCNetG.<lambda>>)

- Parameters

integrand (Integrand) – an instance of Integrand

abs_tol (ndarray) – absolute error tolerance

rel_tol (ndarray) – relative error tolerance

n_init (int) – initial number of samples

n_max (int) – maximum number of samples

fudge (function) – positive function multiplying the finite sum of Fast Fourier coefficients specified in the cone of functions

check_cone (boolean) – check if the function falls in the cone

control_variates (list) – list of integrand objects to be used as control variates. Control variates are currently only compatible with single level problems. The same discrete distribution instance must be used for the integrand and each of the control variates.

control_variate_means (list) – list of means for each control variate

update_beta (bool) – update control variate beta coefficients at each iteration

error_fun – function taking in the approximate solution vector, absolute tolerance, and relative tolerance which returns the approximate error. Default indicates integration until either absolute OR relative tolerance is satisfied.

- class qmcpy.stopping_criterion.cub_qmc_net_g.CubQMCSobolG(integrand, abs_tol=0.01, rel_tol=0.0, n_init=1024.0, n_max=34359738368.0, fudge=<function CubQMCNetG.<lambda>>, check_cone=False, control_variates=[], control_variate_means=[], update_beta=False, error_fun=<function CubQMCNetG.<lambda>>)

Guaranteed Lattice Cubature (QMC)

- class qmcpy.stopping_criterion.cub_qmc_lattice_g.CubQMCLatticeG(integrand, abs_tol=0.01, rel_tol=0.0, n_init=1024.0, n_max=34359738368.0, fudge=<function CubQMCLatticeG.<lambda>>, check_cone=False, ptransform='Baker', error_fun=<function CubQMCLatticeG.<lambda>>)

Stopping Criterion quasi-Monte Carlo method using rank-1 Lattices cubature over a d-dimensional region to integrate within a specified generalized error tolerance with guarantees under Fourier coefficients cone decay assumptions.

>>> k = Keister(Lattice(2,seed=7)) >>> sc = CubQMCLatticeG(k,abs_tol=.05) >>> solution,data = sc.integrate() >>> data LDTransformData (AccumulateData Object) solution 1.810 comb_bound_low 1.806 comb_bound_high 1.815 comb_flags 1 n_total 2^(10) n 2^(10) time_integrate ... CubQMCLatticeG (StoppingCriterion Object) abs_tol 0.050 rel_tol 0 n_init 2^(10) n_max 2^(35) Keister (Integrand Object) Gaussian (TrueMeasure Object) mean 0 covariance 2^(-1) decomp_type PCA Lattice (DiscreteDistribution Object) d 2^(1) dvec [0 1] randomize 1 order natural gen_vec [ 1 182667] entropy 7 spawn_key () >>> f = BoxIntegral(Lattice(3,seed=7), s=[-1,1]) >>> abs_tol = 1e-3 >>> sc = CubQMCLatticeG(f, abs_tol=abs_tol) >>> solution,data = sc.integrate() >>> solution array([1.18954582, 0.96056304]) >>> sol3neg1 = -pi/4-1/2*log(2)+log(5+3*sqrt(3)) >>> sol31 = sqrt(3)/4+1/2*log(2+sqrt(3))-pi/24 >>> true_value = array([sol3neg1,sol31]) >>> (abs(true_value-solution)<abs_tol).all() True >>> cf = CustomFun( ... true_measure = Uniform(Lattice(6,seed=7)), ... g = lambda x,compute_flags=None: (2*arange(1,7)*x).reshape(-1,2,3), ... dimension_indv = (2,3)) >>> sol,data = CubQMCLatticeG(cf,abs_tol=1e-6).integrate() >>> data LDTransformData (AccumulateData Object) solution [[1. 2. 3.] [4. 5. 6.]] comb_bound_low [[1. 2. 3.] [4. 5. 6.]] comb_bound_high [[1. 2. 3.] [4. 5. 6.]] comb_flags [[ True True True] [ True True True]] n_total 2^(15) n [[ 8192. 16384. 16384.] [16384. 32768. 32768.]] time_integrate ... CubQMCLatticeG (StoppingCriterion Object) abs_tol 1.00e-06 rel_tol 0 n_init 2^(10) n_max 2^(35) CustomFun (Integrand Object) Uniform (TrueMeasure Object) lower_bound 0 upper_bound 1 Lattice (DiscreteDistribution Object) d 6 dvec [0 1 2 3 4 5] randomize 1 order natural gen_vec [ 1 182667 469891 498753 110745 446247] entropy 7 spawn_key ()

Original Implementation:

References

[1] Lluis Antoni Jimenez Rugama and Fred J. Hickernell, “Adaptive multidimensional integration based on rank-1 lattices,” Monte Carlo and Quasi-Monte Carlo Methods: MCQMC, Leuven, Belgium, April 2014 (R. Cools and D. Nuyens, eds.), Springer Proceedings in Mathematics and Statistics, vol. 163, Springer-Verlag, Berlin, 2016, arXiv:1411.1966, pp. 407-422.

[2] Sou-Cheng T. Choi, Yuhan Ding, Fred J. Hickernell, Lan Jiang, Lluis Antoni Jimenez Rugama, Da Li, Jagadeeswaran Rathinavel, Xin Tong, Kan Zhang, Yizhi Zhang, and Xuan Zhou, GAIL: Guaranteed Automatic Integration Library (Version 2.3) [MATLAB Software], 2019. Available from http://gailgithub.github.io/GAIL_Dev/

- Guarantee:

This algorithm computes the integral of real valued functions in

with a prescribed generalized error tolerance. The Fourier coefficients

of the integrand are assumed to be absolutely convergent. If the

algorithm terminates without warning messages, the output is given with

guarantees under the assumption that the integrand lies inside a cone of

functions. The guarantee is based on the decay rate of the Fourier

coefficients. For integration over domains other than , this cone

condition applies to (the composition of the

functions) where is the transformation function for to

the desired region. For more details on how the cone is defined, please

refer to the references below.

- __init__(integrand, abs_tol=0.01, rel_tol=0.0, n_init=1024.0, n_max=34359738368.0, fudge=<function CubQMCLatticeG.<lambda>>, check_cone=False, ptransform='Baker', error_fun=<function CubQMCLatticeG.<lambda>>)

- Parameters

integrand (Integrand) – an instance of Integrand

abs_tol (ndarray) – absolute error tolerance

rel_tol (ndarray) – relative error tolerance

n_init (int) – initial number of samples

n_max (int) – maximum number of samples

fudge (function) – positive function multiplying the finite sum of Fast Fourier coefficients specified in the cone of functions

check_cone (boolean) – check if the function falls in the cone

error_fun – function taking in the approximate solution vector, absolute tolerance, and relative tolerance which returns the approximate error. Default indicates integration until either absolute OR relative tolerance is satisfied.

Bayesian Lattice Cubature (QMC)

- class qmcpy.stopping_criterion.cub_qmc_bayes_lattice_g.CubBayesLatticeG(integrand, abs_tol=0.01, rel_tol=0, n_init=256, n_max=4194304, order=2, alpha=0.01, ptransform='C1sin', error_fun=<function CubBayesLatticeG.<lambda>>)

Stopping criterion for Bayesian Cubature using rank-1 Lattice sequence with guaranteed accuracy over a d-dimensional region to integrate within a specified generalized error tolerance with guarantees under Bayesian assumptions.

>>> k = Keister(Lattice(2, order='linear', seed=123456789)) >>> sc = CubBayesLatticeG(k,abs_tol=.05) >>> solution,data = sc.integrate() >>> data LDTransformBayesData (AccumulateData Object) solution 1.808 comb_bound_low 1.808 comb_bound_high 1.809 comb_flags 1 n_total 2^(8) n 2^(8) time_integrate ... CubBayesLatticeG (StoppingCriterion Object) abs_tol 0.050 rel_tol 0 n_init 2^(8) n_max 2^(22) order 2^(1) Keister (Integrand Object) Gaussian (TrueMeasure Object) mean 0 covariance 2^(-1) decomp_type PCA Lattice (DiscreteDistribution Object) d 2^(1) dvec [0 1] randomize 1 order linear gen_vec [ 1 182667] entropy 123456789 spawn_key ()

Adapted from GAIL cubBayesLattice_g.

- Guarantees:

This algorithm attempts to calculate the integral of function

over the

hyperbox to a prescribed error tolerance

over the

hyperbox to a prescribed error tolerance  with a guaranteed confidence level, e.g.,

with a guaranteed confidence level, e.g.,  when alpha=

when alpha=  .

If the algorithm terminates without showing any warning messages and provides

an answer

.

If the algorithm terminates without showing any warning messages and provides

an answer  , then the following inequality would be satisfied:

, then the following inequality would be satisfied:

This Bayesian cubature algorithm guarantees for integrands that are considered to be an instance of a Gaussian process that falls in the middle of samples space spanned. Where The sample space is spanned by the covariance kernel parametrized by the scale and shape parameter inferred from the sampled values of the integrand. For more details on how the covariance kernels are defined and the parameters are obtained, please refer to the references below.

References

[1] Jagadeeswaran Rathinavel and Fred J. Hickernell, Fast automatic Bayesian cubature using lattice sampling. Stat Comput 29, 1215-1229 (2019). Available from Springer.

[2] Sou-Cheng T. Choi, Yuhan Ding, Fred J. Hickernell, Lan Jiang, Lluis Antoni Jimenez Rugama, Da Li, Jagadeeswaran Rathinavel, Xin Tong, Kan Zhang, Yizhi Zhang, and Xuan Zhou, GAIL: Guaranteed Automatic Integration Library (Version 2.3) [MATLAB Software], 2019. Available from GAIL.

- __init__(integrand, abs_tol=0.01, rel_tol=0, n_init=256, n_max=4194304, order=2, alpha=0.01, ptransform='C1sin', error_fun=<function CubBayesLatticeG.<lambda>>)

- Parameters

integrand (Integrand) – an instance of Integrand

abs_tol (ndarray) – absolute error tolerance

rel_tol (ndarray) – relative error tolerance

n_init (int) – initial number of samples

n_max (int) – maximum number of samples

order (int) – Bernoulli kernel’s order. If zero, choose order automatically

alpha (float) – p-value

ptransform (str) – periodization transform applied to the integrand

error_fun – function taking in the approximate solution vector, absolute tolerance, and relative tolerance which returns the approximate error. Default indicates integration until either absolute OR relative tolerance is satisfied.

- class qmcpy.stopping_criterion.cub_qmc_bayes_lattice_g.CubQMCBayesLatticeG(integrand, abs_tol=0.01, rel_tol=0, n_init=256, n_max=4194304, order=2, alpha=0.01, ptransform='C1sin', error_fun=<function CubBayesLatticeG.<lambda>>)

Bayesian Digital Net Cubature (QMC)

- class qmcpy.stopping_criterion.cub_qmc_bayes_net_g.CubBayesNetG(integrand, abs_tol=0.01, rel_tol=0, n_init=256, n_max=4194304, alpha=0.01, error_fun=<function CubBayesNetG.<lambda>>)

Stopping criterion for Bayesian Cubature using digital net sequence with guaranteed accuracy over a d-dimensional region to integrate within a specified generalized error tolerance with guarantees under Bayesian assumptions.

>>> k = Keister(DigitalNetB2(2, seed=123456789)) >>> sc = CubBayesNetG(k,abs_tol=.05) >>> solution,data = sc.integrate() >>> data LDTransformBayesData (AccumulateData Object) solution 1.812 comb_bound_low 1.796 comb_bound_high 1.827 comb_flags 1 n_total 2^(8) n 2^(8) time_integrate ... CubBayesNetG (StoppingCriterion Object) abs_tol 0.050 rel_tol 0 n_init 2^(8) n_max 2^(22) Keister (Integrand Object) Gaussian (TrueMeasure Object) mean 0 covariance 2^(-1) decomp_type PCA DigitalNetB2 (DiscreteDistribution Object) d 2^(1) dvec [0 1] randomize LMS_DS graycode 0 entropy 123456789 spawn_key ()

Adapted from GAIL cubBayesNet_g.

- Guarantee:

This algorithm attempts to calculate the integral of function

over the

hyperbox to a prescribed error tolerance with a guaranteed confidence level, e.g., when alpha= .

If the algorithm terminates without showing any warning messages and provides

an answer , then the following inequality would be satisfied:This Bayesian cubature algorithm guarantees for integrands that are considered to be an instance of a Gaussian process that falls in the middle of samples space spanned. Where The sample space is spanned by the covariance kernel parametrized by the scale and shape parameter inferred from the sampled values of the integrand. For more details on how the covariance kernels are defined and the parameters are obtained, please refer to the references below.

References

[1] Jagadeeswaran Rathinavel, Fast automatic Bayesian cubature using matching kernels and designs, PhD thesis, Illinois Institute of Technology, 2019.

[2] Sou-Cheng T. Choi, Yuhan Ding, Fred J. Hickernell, Lan Jiang, Lluis Antoni Jimenez Rugama, Da Li, Jagadeeswaran Rathinavel, Xin Tong, Kan Zhang, Yizhi Zhang, and Xuan Zhou, GAIL: Guaranteed Automatic Integration Library (Version 2.3) [MATLAB Software], 2019. Available from GAIL.

- __init__(integrand, abs_tol=0.01, rel_tol=0, n_init=256, n_max=4194304, alpha=0.01, error_fun=<function CubBayesNetG.<lambda>>)

- Parameters

integrand (Integrand) – an instance of Integrand

abs_tol (ndarray) – absolute error tolerance

rel_tol (ndarray) – relative error tolerance

n_init (int) – initial number of samples

n_max (int) – maximum number of samples

alpha (float) – signifcance level or p-value